Stables, Boxes and Bastards

Stables, Boxes and Bastards

Terra's flight near the sun and the future of DeFi

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing. Also, never EVER outsource your conviction on an investment.

Stables

Stablecoins are basically tokens on a blockchain that are supposed to track the value of another asset, usually a major currency. The most popular stablecoins in the market are those pegged (or that try to be pegged) to the US dollar on a 1-for-1 basis. This means that the stablecoin in question should always be worth $1 USD, or thereabouts.

Since they’re tokens on a blockchain they can just as easily be transferred from wallet to wallet, without the need for any intermediary, and they give traders/investors a low volatility asset to flock to during turbulent times without leaving the ecosystem. Stablecoin supply has grown enormously since early 2020, to around $180 billion in various USD-linked stablecoins in the market today:

Although they all attempt to track the value of the US dollar, they use different approaches to doing so:

Fiat fully-backed stablecoins: USDT, USDC, and BUSD fall into this category. The way they work is simple. The companies behind the respective coin receive cash in USD and they create (“mint”) the same amount of their respective coin in the blockchain, which can then be used within the crypto ecosystem. Importantly, the companies behind these coins promise that one can always redeem USD, which means that they should always have at least $1 in their bank account for every coin that is out there in the blockchain, in case a holder of the stablecoin wishes to switch back to fiat. They all claim, some with signed attestations, that they hold at least an equal amount of dollar reserves as the supply of the stablecoin. It’s key to note that these stablecoins are centralized, meaning that the company behind the it can arbitrarily create or modify the rules on how they work. Whether this arrangement aligns with the crypto ethos is debatable.

Crypto fully-backed stablecoins: DAI falls into this category. In order to create (“mint”) new DAI, a user must deposit collateral with a value higher than the value of the DAI they want to create. Essentially, every new unit of DAI that is minted is loaned to the user that deposits the collateral. DAI is always over-collateralized. This collateral must be a cryptocurrency accepted by MakerDAO, the decentralized autonomous organization that manages the DAI stablecoin. You can listen to this podcast to learn a bit more about MakerDAO and DAI.

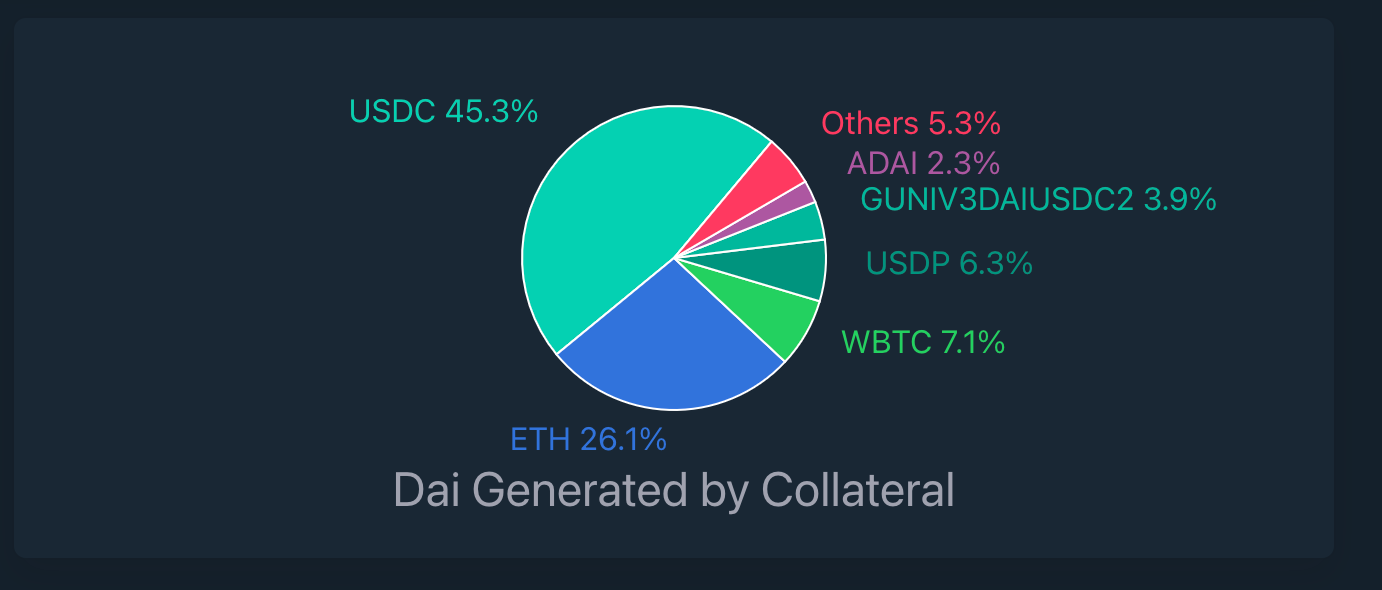

MakerDAO is decentralized, as holders of the MKR token can vote on specific proposals regarding the direction of the protocol, as well as on certain features like the stability fee. Although it’s worth mentioning that over 45% of collateral is USDC, a centralized stablecoin:

Algorithmic stablecoins: UST, and other smaller stablecoins such as FRAX and FEI, falls into this category, and this is the main category I want to discuss today.

At their core, algorithmic stablecoins seek to maintain a 1-to-1 peg with another asset (again, in the vast majority of cases this asset is the US dollar) without the need to hold dollar reserves backing the stablecoin. How?

Matt Levine, a great writer for Bloomberg explains it best:

“Here is how an algorithmic stablecoin works. You invent two tokens, call them Dollarcoin and Sharecoin. You list them on the crypto exchanges. Sharecoin trades for whatever price is determined by supply and demand. It might be $0.01 per Sharecoin, or $1, or $100, who knows. But Dollarcoin is supposed to trade at $1. If it trades at $0.99, you have some automatic process in which you print more Sharecoins and use them to buy Dollarcoins until it is back to $1. If it trades at $1.01, you have some automatic process in which you print some more Dollarcoins and use them to buy Sharecoins until it is back to $1. The result is that Dollarcoin is firmly pegged to the dollar. The process is sometimes compared to algorithmic central banking, where the central bank maintains the value of the currency (Dollarcoin) by adjusting its supply.” - Matt Levine

The specific mechanism highlighted above varies slightly depending on the project. However, as Matt points out it relies on “Sharecoin” always having some value.

The growth of UST specifically has been massive, from $2 billion to $18 billion in one year:

Given the role that LUNA plays in maintaining UST’s value at $1, growth in UST via price increases or quantity increases thanks to more demand reverberates into the LUNA price. If UST demand goes up, LUNA price goes up because it is burned to mint more UST. You can go here to learn more about how the LUNA-UST mechanism works.

The main way Terra has “bootstrapped” demand for UST is through Anchor, a borrowing & lending app where UST holders can deposit their UST and, until recently, earn 19.5% fixed interest per year. A large part of the interest came from the protocol’s reserve, funded by large Terra backers (the Luna Foundation Guard, or “LFG”). This is, of course, not sustainable.

Some view this continuous topping up of the reserve in order to maintain an organically unsustainable interest rate as marketing spend to increase UST adoption and, therefore, the growth of the entire Terra ecosystem. Some would call it a ponzi. At the very least it’s an extremely common practice in DeFi. Almost every project offers juicy, albeit unsustainable, rewards to early users in order to boost acquisition and TVL.

On LUNA and UST, if you really understood the implications of Matt Levine’s explanation you probably realized that there is also the risk of a death spiral in which selling UST triggers selling of LUNA which reduces trust in the mechanism which leads to more UST selling and… you get the gist. The bearish argument is neatly summarized in this article.

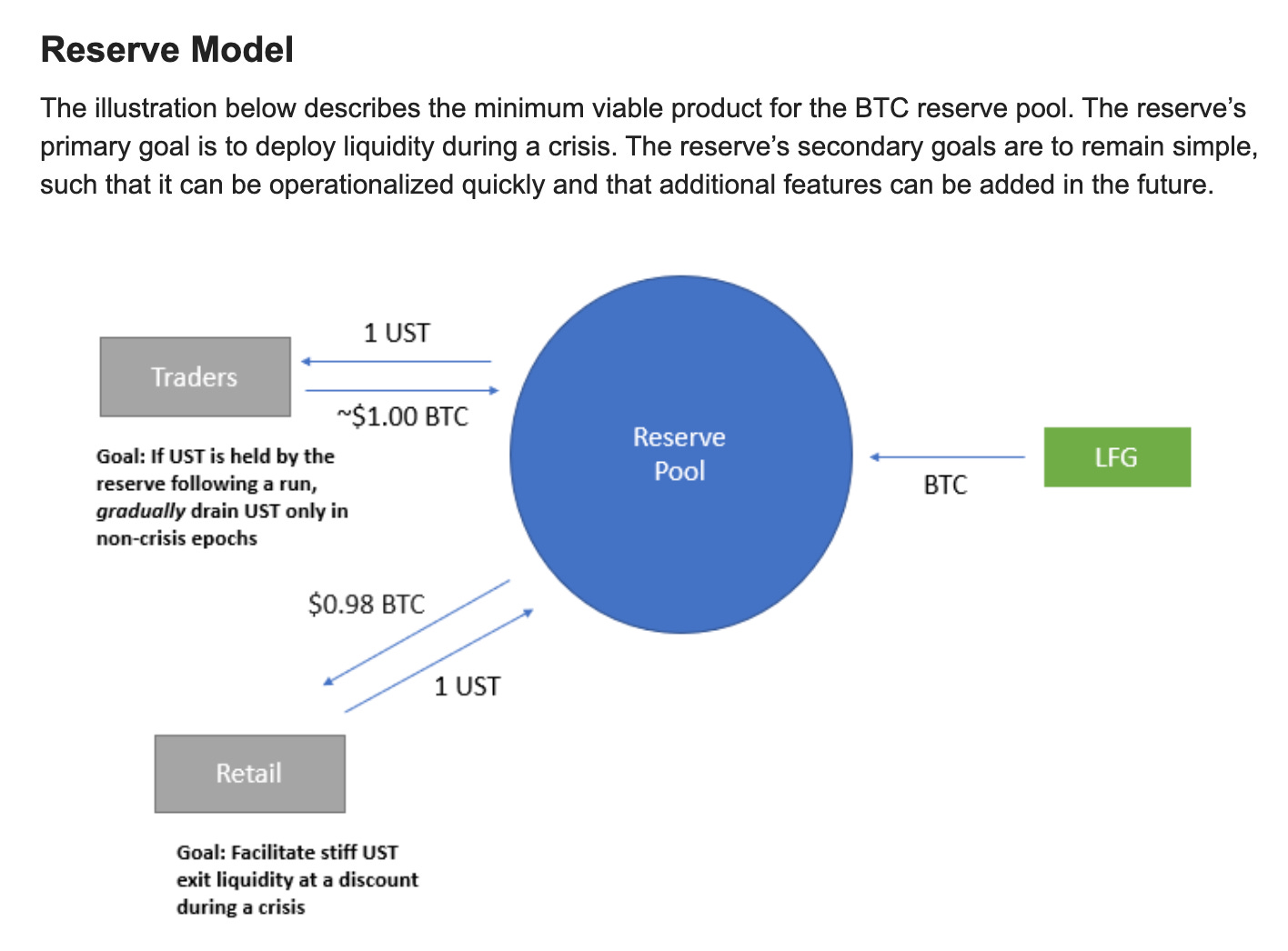

They’ve recently added another feature to the UST experiment however: they purchased billions of dollars worth of Bitcoin to provide liquidity for the protocol during a crisis:

Regardless of what you think its value is, Bitcoin is decentralized, trustless, and established enough. Having it indirectly backing your algorithmic stablecoin makes your stablecoin a bit less algorithmic though. Also, Bitcoin is many things. Stable is not one of them. Sometimes I wonder… I guess it’s nice for Terra bulls that the LFG stands behind UST ready to help it survive, but doesn’t the fact that they have to do so defeat the purpose? Honest question.

I’ve been writing this on Monday, May 9th, and what do you know, the UST peg is under HEAVY pressure as I type:

And LUNA has been puking the past few days:

One of the main issues I see is that there is a lack of organic and productive demand for UST (and other stablecoins tbh) beyond trading or depositing it in a smart contract with artificially high interest rates. It’s cool that you can send it anywhere at almost no cost with incredible speed, but if you can’t then use it in the real economy then utility is quite low.

Terra hasn’t really focused on generating this productive demand for UST. If you rely solely on paying high rates, in an industry in which high rates are magically generated, then there’s no reason why your stablecoin won’t be replaced by another one. Using Warren Buffett speak, there is no “moat”. Sure, now it’s partially backed by Bitcoin, but it seems all that is doing is bringing the rest of the market down with it.

At least, we get to see all of this play out in real time. Gotta give it to Terra and UST, they grew bigger and lasted longer than most…

DeFi (as I saw it)

When I first heard about DeFi and began researching some of the projects being built I was beyond excited. Finance is an industry with too many intermediaries, filled with shady practices, and ripe for disruption.

Let’s not even talk about the situation in many emerging countries where citizens are slaves to local governments’ self-destructive policies. Nowhere is the promise of crypto and DeFi more necessary than in countries such as Argentina and Turkey, for example. Yes, fiat works well if your government is not completely hell-bent on destroying your purchasing power and/or if your country (and therefore your currency) enjoys a privileged position in the global financial order. It’s easy to dismiss crypto from the developed West when you can take these things for granted. That is, until you can’t. Free movement of capital is not a God-given right…

It’s also partly about control, which is why I believe Western institutions are trying to undermine crypto in developing economies.

Providing access to efficient and inclusive financial services through trustless, decentralized structures while avoiding reliance on corrupt, overreaching institutions is a worthy mission. The potential is enormous, but it seems we have made little progress from what it is to what it could be. Perhaps part of the problem is that we keep selling it as what it could be, instead of actively working to make it so. It’s a bit something like this:

Good Ponzi, Bad Ponzi

I wasn’t really surprised when I heard Sam Bankman-Fried basically compare yield farming to a magic box. Ponzis are a meme in crypto. For some time now, the difference between “good” projects and “bad” projects has been merely how well the ponzi was structured. Every other aspiration around the crypto vision has been left behind, from decentralization to individual sovereignty. Most focus has been in structuring a good ponzi in hopes that it would eventually become sustainable, stop being a ponzi, and revolutionize finance. Eventually, at some undefined point in the future…

But it’s hard to revolutionize finance when all the effort is directed to propping up the ponzi and not on creating real utility. There’s a point in which inserting a project’s token into the dynamic stops being a marketing incentive and starts being a lazy counterproductive attempt at staying relevant.

I was really excited about the idea of decentralized money that’s not beholden to politicians’ decisions. I still think there’s an enormous potential in the space (isn’t there always?).

The pain points are still very much there.

The pandemic and the return of inflation have continued the erosion of trust in public officials and in traditional institutions that began to accelerate after the GFC, and I don’t see this getting better anytime soon.

Governments in the West are, in general, turning towards more surveillance and arbitrary social and financial controls. Add to this the list of usual authoritarian suspects elsewhere and you’ve got a nasty pile of dong.

The financial services industry continues to be filled with inefficient, extractive middlemen.

Even if ultimately unsuccessful, it’s hard to argue that trying to materialize the vision of efficient and inclusive financial services for everyone is not worth the effort to at least try. And I would actually agree with you if you said, “yeah, but we don’t really need crypto for that.” At least not as it currently exists.

Crypto in general needs to refocus its purpose. It’s become a bastardized version of what it originally intended to be.

It’s natural that in order to gain legitimacy the space has engaged more and more with traditional financial markets. The listing of BTC and ETH futures and the fight to approve a Bitcoin ETF in the US have been the most prominent efforts at providing legitimacy for crypto in traditional markets. But these efforts have also contributed to a loss of identity for the industry, enmeshing it into Wall Street’s machine. At this moment, crypto is tied to the hip with equity markets. While this seems obvious for people who understand markets and risk, it is a bit disappointing for those of us that also expect more from the space. Ben Hunt sorta made this point come to life with words in an article on Bitcoin from April 2021. Highly recommend it.

Unfortunately, we’re stuck in a world in which the pain points I mentioned above are not as relevant as whether the Federal Reserve printer goes brrrr or not. Crypto and DeFi are bastards precisely at the time when they should be capturing a market ripe for the taking. Macrodesiac, as per usual, did a great job at outlining why crypto will be redefined in the years to come. We’ll see. There is still time for a DeFi redemption arc.

Thanks for reading! Hope you enjoyed and got a kick out of it! Until next time!