Real Men Have Fabs

Taiwan Semiconductor Manufacturing Company (TSMC)

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

I do not own TSMC shares as of the time of writing, so please don’t take what you read as investment advice. I wouldn’t call this a thesis either. Always do your own research before making any decisions to buy or sell an investment.

Intro

There are two things about semiconductors I’m certain about: 1) they are, and will continue to be, one of the essential cogs in the world’s economic machine, and 2) it’s a tough industry to fully understand. The semiconductor industry is fast-changing, and held together by a complex web of relationships that stretch across the world.

While there are a few areas I consider especially interesting, such as Electronic Design Automation, and Equipment (particularly ASML), for today we need to have a basic understanding of the following 3:

Fabless Design: these companies design chips using various software tools and IP, but don’t manufacture them. Some companies, such as Nvidia, design chips for 3rd party customers, while others, like Apple, design chips for their own hardware products. Different fabless designers tend to specialize in designing different types of chips.

Foundries: also called “pure-play” foundries, these companies manufacture chips designed by clients. They set up and own the factories (called “fabs”), and are in charge of production processes. They don’t compete with fabless designers, an important point. Foundries are generally able to manufacture various different types of chips, so they’re not limited to serving only one kind of fabless designer.

Integrated Device Manufacturers (“IDMs”): finally, IDMs are like a combination of 1 and 2. They both design and manufacture chips for 3rd parties, so they also own their fabs. Different IDMs can operate in different markets in the semiconductor industry. For example, Micron focuses solely on designing and manufacturing memory chips, Texas Instruments focuses on analog chips, and Samsung focuses on both memory and logic chips.

Before 1987, IDMs were the norm as it was considered a competitive advantage to operate throughout the value chain. “Real men have fabs” was the saying that illustrated this era best. Until TSMC came along…

Brief History & Facts

The Taiwan Semiconductor Manufacturing Company was born in 1987 in, you guessed it, Taiwan. It was an initiative of the Taiwanese government, who tasked Morris Chang, a renowned former Texas Instruments executive, to build a successful semiconductor firm in the country. The government put up half of the initial investment and left the business model and operations to Morris.

Fun Fact: Morris Chang received no equity in the venture. He did however, buy shares of the company on his own accord once he saw they were on to something. He’s now a billionaire. Talk about conviction in what you’re doing.

Back then it was believed that the right way to operate a semiconductor company was to both design and manufacture chips in-house. One of the main problems that fabless design companies had, even though the number of such firms was quite low, was that they always had to go to IDMs to get their chips manufactured. Since IDMs also designed their own chips, it’s easy to see how getting up close access to a competitor’s technology helped them further their lead.

Morris thought things could be done differently and he pioneered what is called the “pure-play” foundry. He intuitively understood that if you were able to achieve scale relatively quickly to take care of the economics, operating a “pure-play” foundry would give TSMC an important advantage in regards to gaining customers’ trust. Morris was CEO of the firm from 1987 until 2005, when he handed the reigns to Rick Tsai. He then returned in 2009 for a second stint and worked as CEO until his retirement in 2018 at the age of 86.

The company listed on the Taiwanese Stock Exchange in 1993. It also became the first Taiwanese company to be listed in the New York Stock Exchange in 1997. The price in October of 1997 was $4.2 per ADR (“American Depositary Receipt”). Today, TSMC is the 11th largest company in the world, trading at over $90 per ADR, with a market cap of $483.85 billion.

TSMC scored what is probably the biggest win in their history when it struck a deal with Apple to manufacture the iPhone’s chips in the early half of the 2010s. This resulted in TSMC gaining a strong foothold in the smartphone market and nailing the switch to mobile technology that would define the decade.

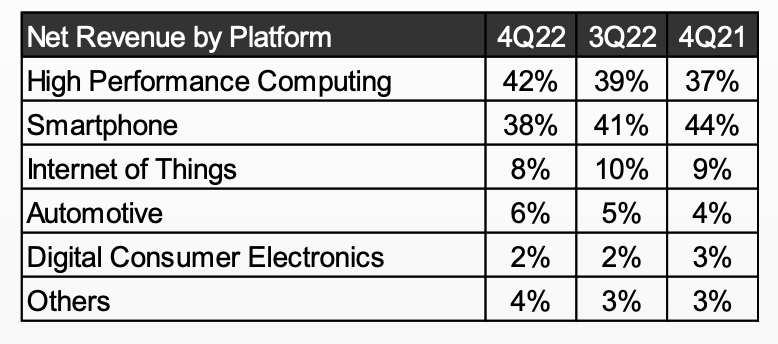

As of 2022, the company manufactures chips for fabless designers, as well as for IDMs in need of additional capacity. They operate across 5 platforms:

Smartphones - pretty self explanatory.

High Performance Computing (HPC) - PCs, tablets, game consoles, servers, etc.

Internet of Things (IoT) - smart wearables, speakers, health devices, home automation devices, surveillance systems, smart manufacturing, etc.

Automotive - also pretty self explanatory.

Digital Consumer Electronics - TVs, set-top boxes, digital cameras, cordless phones, etc.

Out of these 5 platforms, Smartphones and HPC are by far the most significant accounting for 80% of total revenues.

Jensen Huang, the president and CEO of Nvidia, illustrated best just how wide TSMC’s reach is 👇🏽

“This is a company that manufactures something, that I have the utmost confidence, that right now as I speak that every single person in this audience has in his possession.”

If you own a smartphone, computer, car or other electronic device, chances are that there’s a TSMC-manufactured chip in it. If you want to get a better idea of the sheer importance of TSMC to the global economy, as of 2021 the company accounted for 26% of the worldwide semiconductor market, excluding memory.

Business Model & Competitive Advantage(s)

Innovation

The semiconductor industry is constantly evolving and innovating, so companies need to continuously invest and reinvent themselves in order to stay ahead. The key factor that influences the degree of technological advancement in chip design and manufacturing is the process node. This refers to the size of each individual transistor on a chip. The smaller the process node the better as this allows for more transistors within a given area surface. The more transistors that can be fit in a given surface the higher the performance. This is an oversimplification, but it’s generally true. Currently, the most advanced process node at scale is the 5nm (nanometer), which represents a good chunk of TSMC’s revenue.

Both TSMC and Samsung have begun production of 3nm process nodes, while American giant Intel is investing heavily to play catch up. Intel is a good illustration of what happens when you take your eye off the ball in regards to technological development in the chip industry, but it’s hot on the heels of both TSMC and Samsung, at least if you believe management’s roadmap updates.

TSMC needs to constantly stay on its toes, lest its advantage be eroded. This is why they spend substantial amounts on R&D each year. Since 2017, TSMC has invested $19.5 billion into R&D. It’s not exactly an apples to apples comparison given the different business models, but Intel has spent over $75 billion during the same time period, and it still hasn’t been able to catch up. Operating at the leading edge is expensive and requires unique focus.

Capital Intensity

Semiconductor manufacturing is a capital intensive business. Building a semiconductor fab is estimated to cost between $15 billion and $20 billion. That’s a lot of dough. TSMC has spent an average of ~40% of annual sales in capital expenditures during the past 5 years, with the 2021-2022 numbers coming in closer to 50% of sales. While I think most of this can be called growth capex, TSMC operates in an industry that requires it to continually invest increasing amounts of capital to maintain its leadership position. Even among other pure-play foundries, TSMC invests more👇🏽

Only a handful of companies in the world have the financial wherewithal to spend so much money on these highly sophisticated facilities. Accumulating the expertise to operate them efficiently is also no walk in the park. This gives incumbents good protection from new entrants into the pure-play foundry industry. Contrast this with fabless design, where lower barriers to entry are the norm due to the lower initial capital requirements. TSMC currently has 12 live fabs, out of which 10 are in Taiwan, 1 in China, and 1 in the US. The company is also currently moving forward with plans to build two additional fabs in Arizona and one in Japan.

Emphasis on the Customer

The company’s 4th core value is “Customer Trust”, and it’s central to the success of their business model. I already touched upon the advantages of the pure-play foundry model when it comes to building and maintaining positive customer relationships. They don’t, and will not, compete with their customers. TSMC has never had an issue with working in the background and letting their customers shine in the spotlight. This allows them to focus on what matters, driving innovation and efficiency gains in the manufacturing process, working closely with their customers to continue developing best-in-class chips. This strength that their commitment to customers provides to their brand is also why TSMC needs to spend such little amounts in sales & marketing activities. For the 5 years up until 2021 (latest FY for which I have data), TSMC spent an average of 0.56% of revenues on S&M. Contrast this with the much higher average of 8.23% of revenues for R&D during the same period.

Their ability to do this also derives from a key risk for their business. TSMC’s business is heavily concentrated in a handful of large customers. From their 2021 20-F 👇🏽

Their largest customer is, unsurprisingly, Apple. This of course means that TSMC is heavily exposed to demand fluctuations for Apple products, and issues in the Cupertino company could reverberate back to TSMC. However, the Taiwanese company is no stranger to losing revenue from large customers. You’ll notice Hi-Silicon in the table below went from 15% of revenues in 2019 to 0% in 2021. Hi-Silicon is owned by Huawei, which was hit by strong sanctions from the US government that restricted its access to chips. TSMC was able to continue growing revenues, profits and cash flows without much hiccup. Granted, helped by a pandemic that exponentially increased demand for technology hardware.

Still, losing Apple would be a much rougher hit, but it seems ties are only getting stronger:

In any case, TSMC is the kind of company that will never act to jeopardize their customer relationships. Of course, it’s safe to assume that customers will reciprocate only as long as TSMC is able to maintain excellence in terms of manufacturing processes. At the end of the day, it’s hard to imagine many North American customers being super comfortable with such a key step in their value chain located in such a hot geopolitical region (more on this later).

Scale & Efficiency

Operating and investing at the leading edge is not the only requirement for success. Economies of scale is the key to growing a successful foundry business. As scale grows, so does manufacturing expertise, making processes more efficient and reducing costs, which in turn attracts more customers, increasing scale. It’s not a bad flywheel once you get it going.

Ramping up a new process node costs a decent amount of money, especially before you’re able to produce them at massive scale and achieve those efficiency gains. This is why it’s important for foundries to optimize yields and capacity utilization. In regards to 3nm nodes, the latest to start production on a massive scale, TSMC is apparently performing much better than Samsung, the only other company manufacturing 3nm nodes, in terms of yields.

Since semiconductor manufacturing is a business with a large proportion of fixed costs, increased scale and efficiency can translate to very impressive gains in terms of margins and profits. Of course, this can also make the business more vulnerable on the downside when demand falls.

Financial Analysis

Growth

During the past 5 years, revenues have grown from $33.7 billion to $73.6 billion in 2022, for a CAGR of 16.9%. Throughout that same time period, operating earnings grew at a CAGR of 23.6% thanks to strong operating leverage.

Margins

Gross profit margins were 59.6% during 2022, but the 5-year average is closer to 51.8%. Operating margins are also phenomenal at a 5-year average of 41.1%. I expect these margins to normalize at levels closer to the averages, especially since 3nm is just ramping up and 2022 was a year with many tailwinds, such as FX rates, and probably peak of the cycle.

TSMC is clearly best-in-class when it comes to the foundry business:

Free cash flow margins are much lower at ~20% for the 5-year average and ~23% for 2022. Net income has been consistently more than 1.5x higher than free cash flow during the past 4 years, which translates to a very poor cash conversion ratio. This goes to show just how capital intensive the business is. Still they have generated almost $52 billion in free cash flow from 2017 until 2022.

Debt

The business consistently operates with a net cash position. Even though it has significantly increased its debt from $6.4 billion in 2019 to $27.8 billion in 2022, Net Debt-to-EBITA has actually decreased thanks to higher cash generation. Current Net Debt-to-EBITA stands at -0.43, so there’s room for additional leverage, if needed. Even with a drop-off in free cash flow in 2023, I’m fairly certain the company will get through the current investment cycle in good shape.

Capital Allocation

Even though capital expenditures take up a big chunk of the company’s cash flows, ROIC is quite impressive. 5-year average ROIC, which varies a bit depending on how it’s calculated, is ~22%-23%. It’s clear that the internal reinvestment opportunities are very attractive as the chip market continues to grow and additional capacity is required, not to mention some attractive subsidies being offered by governments across the globe. On top of the two Arizona fabs, TSMC is also building a new fab in Japan under a joint venture with Sony and Denso, with the Japanese government putting in 40% of the total cost.

These reinvestment opportunities are why TSMC has not made any acquisitions since 2015. They also prefer to return cash to shareholders in the form of a dividend. They’ve paid out $43.5 billion to shareholders in dividends during the past 5 years. That is almost 85% of their free cash flow. Given the company’s strong financial position, some opportunistic share repurchases could have created tons of value at certain prices, such as during November of last year, but the little repurchases they do are solely to offset dilution from stock-based compensation. TSMC is one of those rare tech companies where such compensation practices are almost non-existent. During 2021, SBC amounted to a whopping $280k (yes, thousand).

Valuation

TSMC stock is trading at 12.37x NTM EV/EBIT, under it’s 10-year average of ~14x. It also trades at ~16.4x NTM earnings, slightly under its 10-year average of ~17.50x. It traded at a more than 10-year low of 8.11x EBIT and 10.17x earnings as recently as early November 2022, but it has since rebounded strongly. Free Cash Flow yield looks a bit less attractive at only 2.6%.

Doing a quick reverse DCF on a 5-year horizon, assuming a 12.5% discount rate and a 15x exit FCF multiple, I get an implied free cash flow growth rate of ~7% from 2022’s number. This actually seems quite sensible considering that 2022 was probably the peak of the cycle for TSMC and the next couple of years should be a bit rougher. The multiple is also a little conservative, at least in comparison to what it has historically been.

Risks

Client Concentration

Relying so much in a small number of customers is always a tricky position to be in. A large issue with Apple, Mediatek, AMD or Nvidia, for example, could result in problems for TSMC. So could losing one of these customers to a competitor. On the flip side, TSMC’s customer relationships are one of the strongest aspects of the company’s business model. These relationships have been nurtured for some time and the level of alignment needed to successfully design and manufacture high-end chips is very high, to the point its developed into an ecosystem. Still, semiconductors are already cyclical and such a high degree of concentration can lead to volatile results.

Loss of Technological Advantage

Clearly, success in the semiconductor industry requires companies to constantly stay on their toes and to never get their eye off the ball. History is filled with semiconductor companies that failed to adapt and either disappeared or are a shadow of their former selves. TSMC currently enjoys a position of leadership, but staying there will require tons of capital and solid execution. I don’t think anyone would have expected Intel to be in the weak position they’re in now back in 1999. Shit happens. In my opinion, it would take either a paradigm shift, such as moving from mobile to the next big platform where everyone starts from scratch, or a fumble of gigantic proportions for TSMC to lose their current position.

The Biggie: Geopolitical Risk

I don’t want to spend too many words here, simply because an invasion of Taiwan is such a hard event to try to predict. Is it a major risk? In terms of its potential effects, yes. In terms of probability, I would say no. I think China has: 1) taken a close look at the backlash of Russia’s invasion of Ukraine and realized going for Taiwan would be foolish, and 2) too many problems to fix at home (demographics, pollution, the economy, etc.) to spend valuable resources on a quest with questionable benefits for China’s prosperity. In any case, if China does invade Taiwan I think there are very few companies that would do well and the magnitude of the conflict would most likely result in dire consequences for the entire world.

Verdict

TSMC is a fantastic company and it will most likely continue benefiting from the tailwinds of secular semiconductor demand as the leader in a business with high barriers to entry. It has a nice competitive advantage, superior margins, solid returns on capital and a good balance sheet. In regards to capital allocation, I do think that the management does a good job at recognizing the opportunities in their core business and invests accordingly. It’s a capital intensive business though, which is not ideal, but it does generate a respectable amount of free cash flows. It’s at a decent valuation considering the quality of the business, but I don’t think it’s incredibly cheap at these prices however. At the end of the day, TSMC does come with added geopolitical risks. I think you were getting paid for that back in November, but now I’m not so sure. I’ll add it to my watchlist and follow the business closely. Maybe 2023 will surprise us with some more fear.

Resources

If you want to learn more about TSMC you can go here:

Sravan Kundojjala was some great insights on the semiconductor industry in general

Stratechery has some great articles about TSMC (and semis in general)

Finally, I take the data for my financial analyses from TIKR Terminal.

Hope you have found this post useful!