My Investment Strategy

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

In some of my previous posts I have touched upon certain topics I will mention here, so it might be worth (re)visiting those posts to get a more comprehensive view of my opinion on these concepts. I’ll point you to them when necessary. In this post I will summarize my investment strategy, breaking down my philosophy as well as the details of my process. The strategy below fits my goals and works for my particular style, but it probably does not fit everyone. Keep that in the back of your mind as you read. One of my objectives here is to think deeply about the various elements and continuously evolve and improve. Hope it’s useful in some way to you as the reader!

Why Invest in Stocks

Before starting, I do have to say that I invest in assets other than equities. I have some holdings in a few cryptocurrencies, a little bit of physical gold, and in the future, once I’m able to, I want to invest in real estate. But equities are and will continue to be the most important part of my investment strategy, by a mile.

Equities (shares, stocks, however you want to call them) are portions of ownership in a business. And investing in businesses has an inherent advantage over investing in every other asset class: businesses can compound capital for you at high returns.

If you invest in bonds or real estate, you receive income on a regular basis. You then have to actively work to reinvest this income into opportunities that offer solid returns. When you invest in a business, the management team reinvests your capital for you. Furthermore, the returns on capital available for businesses is generally much higher than rates available to you and me. Businesses can invest at much higher rates than can your typical equity (or multi-asset class for that matter) fund manager. If your goal is to increase your net worth, investing in businesses that reinvest capital into high return opportunities is, in my view, a superior approach. Of course, you can have other goals (such as investing for income), and in these cases perhaps other assets can have an important role in your portfolio.

Concentration vs Diversification

“We would propose that if knowledge is a source of value added, and few things can be known for sure, then it logically follows that owning more stocks does not lower risk, but raises it.” - Nick Sleep

Diversification is protection against ignorance. That said, being ignorant is not necessarily a bad thing, as long as we recognize it and act accordingly. Some people do not have the time to intensively research businesses. That’s fine. In those cases, diversification through an index fund is a much better approach than trying to pick stocks. I wrote about the benefits of indexing here. At the end of the day, most active investors that pick stocks end up underperforming the market.

If the goal is to outperform the market, then diversifying beyond 20 or so companies is a fool’s errand. There’s sound research showing that marginal diversification benefits tend to drastically fall after a portfolio exceeds 20-25 stocks.

Running a concentrated portfolio dos require effort and time. So if you’re going to dedicate yourself to building such a portfolio, why would you dilute your best ideas? Most people don’t have more than 20-25 really good investment ideas in their entire lifetimes. I can tell you without shame, I don’t have many truly good investment ideas every year. Having a profound understanding of more than a certain number of companies becomes prohibitive as an individual investor.

Additionally, unless you’re managing money professionally and are in the unfortunate situation of having investors who constantly nag you, there is nobody forcing you to act. You can patiently wait until you get a pitch that falls right into your sweet zone. Then when something does fall into your sweet zone it probably pays to follow Charlie Munger’s advice: “Use a shovel, not a spoon”.

While I resolutely agree with the argument for concentration, I do recognize the power of indexing for those that feel more comfortable diversifying and can’t (or don’t want to try to) outperform the market. There’s also nothing wrong if you prefer to research businesses and don’t feel comfortable owning less than x number of stocks. Humility is an important trait to have when investing. No one is going to achieve a 100% success rate. However, I subscribe to Buffett’s thinking:

“We believe that a policy of portfolio concentration may well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying into it.” - Warren Buffett

My Investment Philosophy

I wrote about the importance of an investment philosophy here. In that post I touched upon some of the key common traits of a successful investment philosophy. Here I expand on those traits and add the rest that compose my own.

Long-term Orientation - as I mentioned in the post linked above, the average holding period of a stock is now <6 months. Wall Street views more than 1 year as a long-term investment horizon. There is a short-term thinking epidemic in financial markets, exacerbated by the temptation for market timing. In my view, focusing on a long-term horizon (10-15 years+) can be a huge competitive advantage for investors. A long-term orientation grounds every decision I make when I invest.

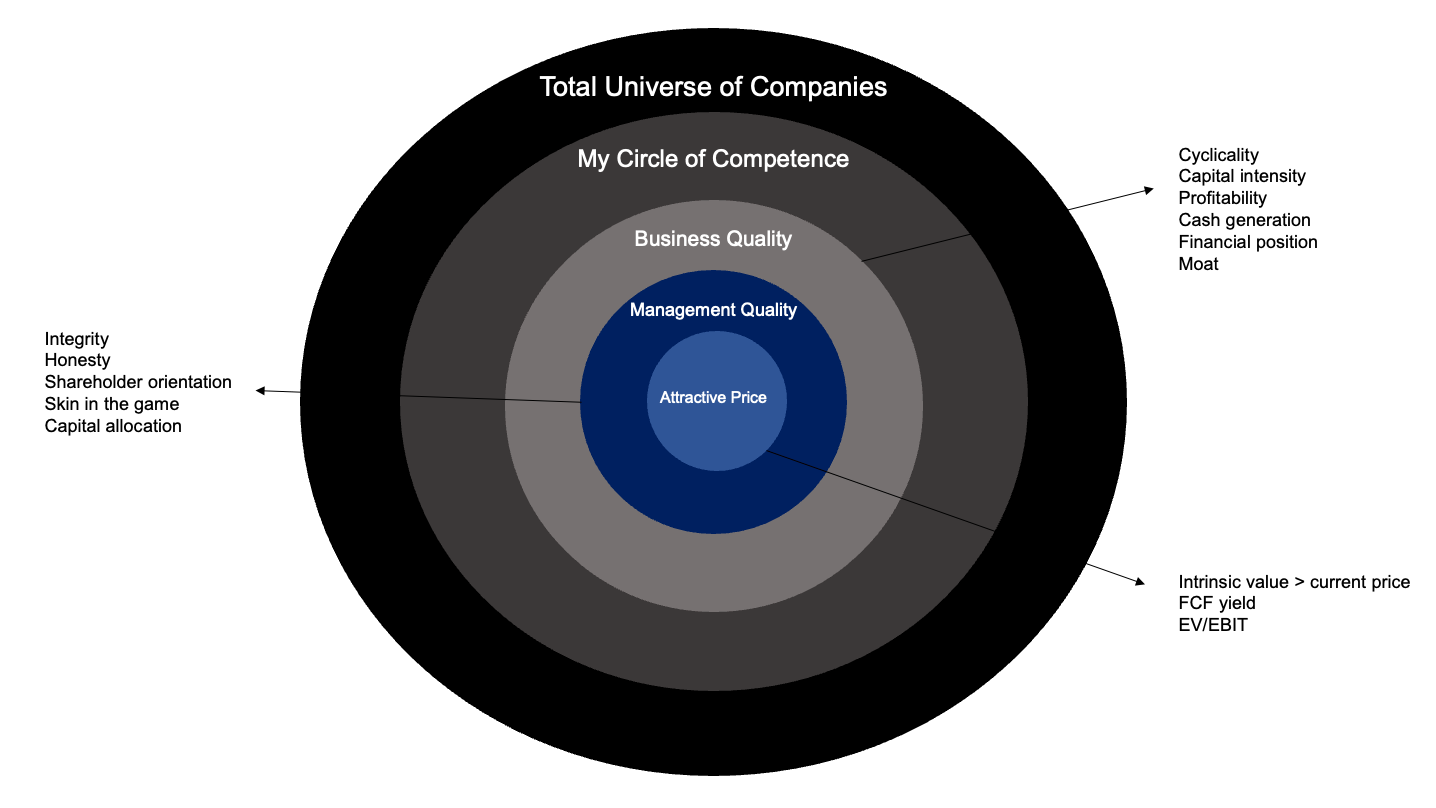

Intellectual Honesty - I wrote about the concept of the circle of competence here. Being brutally honest about what you know and what you don’t know is essential for success, as is staying within the perimeter of what you know. I stay within the boundaries of what I know today, while actively working to expand those boundaries.

Analytical Rigor - today’s markets are filled with noise, from news headlines to quarterly earnings, that distract investors from thinking about the fundamentals of businesses. Financial markets tend to be very efficient at analyzing quantitative data, but good qualitative insights, stemming from reading, thinking, and talking with stakeholders, remain an edge. Everyone can do the math for investing, it’s not hard. I try to develop an analytical advantage because I think opportunity exists there.

Sitting down to read and think is a skill that seems to be forgotten these days. Emotional control - volatility is often seen as an adequate measure of risk. I think volatility does represent risk for those investors that are not emotionally prepared for the ups and downs of markets. For the prepared investor, volatility is opportunity. Remaining unemotional during your research process and in the face of market volatility is a pre-requirement for success. This allows you to actually be greedy when others are fearful, instead of panic-selling. This is probably the biggest advantage I (and other non-professional investors) have over professional money managers. I think Rob Vinall explained the necessary mindset best:

“When I started managing the fund <RV Capital>, I knew there would be periods of poor performance - no manager is immune to them. The trick is to manage through them with sufficient equanimity to be able to continue to function rationally, but not so much equanimity to be oblivious to the feedback the market is giving you.” - Rob Vinall

Focus - in investing, there are important and non-important factors. Some of these factors are knowable, while others are unknowable. One of the keys of investing is to focus on those factors that are both important and knowable. Macroeconomic and geopolitical developments are important, but they’re unknowable by most, so spending tons of time thinking about macro forecasts seems to me a waste of time. My focus is on analyzing the fundamentals of a business. I do try to pay attention to cycles, something I learned from reading Howard Marks, but this relates more to trying to identify where we are in a cycle (economic, credit, etc.) rather than making predictions.

Most people’s track record of forecasting macro is extremely poor. Consistency (w/ continuous improvement) - there are few things more dangerous than flip-flopping. It’s imperative to focus on what works for you. Consistency in your analysis and actions is non-negotiable. I record all of my analysis and decisions, constantly making sure I’m staying true to my goal and improving the process. Needless to say, but if you don’t enjoy the process it will be incredibly hard to stick with it.

Good Businesses

It seems obvious to try to invest solely in good businesses. Funnily enough, a large number of investors (professional and amateur) can’t resist the temptation to try and make money out of bad businesses. These investors presume that, if undervalued enough, they can buy a business and make a profit once this price-value gap closes. To be completely fair, money can be made in such a way. But it’s extremely tough to do consistently. Other investors focus solely on companies that pay high dividends. In both cases, with low quality businesses, the company’s value tends to erode while you wait for the price-value gap to close or the dividend payouts to occur.

So, what’s a good business for me? That would be a business with the following characteristics:

Low cyclicality - I prefer businesses with fortunes that fluctuate less during an economic cycle. I really like companies with recurring revenues and cash flows because timing the cycle is less of an issue.

Potential for growth - I try to search for companies operating in markets with strong tailwinds. These businesses are usually able to ride these tailwinds and generate healthy levels of growth. While not impossible to make money investing in stagnant businesses, it’s certainly harder to find relatively good prospects in declining markets. Some companies are also fantastic at growing through acquisitions. This is harder (i.e., requires a lot more skill from management) than simply operating in a growing market, but I won’t discard them for analysis.

High profit margins - I tend to prefer businesses with high gross and operating margins. These businesses are better-able to weather times of increasing costs. For companies that reinvest a lot through the income statement, an analysis of the unit economics and cost structure can provide insights as to the future profitability.

There is a special case which merits a mention here. There are some businesses that exhibit scale economies shared. These are businesses that do tons of small things right, save on costs and pass on those savings to customers. Think Costco, Amazon and Southwest Airlines. These businesses tend to have small profit margins, but the small margins themselves are an output of a strong competitive management vis-a-vis competitors. In these cases, I don’t mind low margins.

High cash flow generation - Cash is the life blood of a business. Ultimately, ownership in a business gives you a right to the company’s free cash flows. Of course, many businesses are not optimizing for free cash flow today but rather reinvesting into growth opportunities. This is why I highlight the potential cash generation. For those businesses already generating profits, cash conversion levels are very important.

Capital light - The best businesses are those that do not need tons of capital to operate and grow. In order to obtain high returns on reinvestment, requiring less dollars of capital to generate one dollar of return is a huge advantage.

Solid financial position - This point is one of personal preference. I favour businesses with more conservative balance sheets, simply because it helps me sleep better at night. I also hope it helps the management sleep better at night. Net cash positions are good, but relatively low levels of leverage (Net Debt/EBITA) and a solid interest coverage (EBITA/Interest Payments) also work. I often tend to look closely at the debt maturity schedule as well.

Good management - I believe the effect of bad management on a great business can be extremely detrimental, so I favor finding management teams that are honest, sharp and that view shareholders as partners. Most CEOs are not good enough to be a competitive advantage for the business, but some are. I’ll settle for honest and able. Extra points for skin in the game.

Mindful capital allocation - To some degree this is also an evaluation of management. In my view, the main job of a CEO is to ensure capital is directed to the highest return opportunities, whether this is reinvesting it for organic growth, acquiring other companies, paying dividends or repurchasing shares. CEOs and management teams that successfully do this create the most value. To do this, some form of rebelliousness is necessary to ignore what Buffett calls “the institutional imperative”.

Widening moat - A moat is a sustainable competitive advantage that helps protect a business from attacks by competitors. Some of the moats I keep an eye out for are: a strong brand, network effects, high switching costs, low cost providers, and company culture. Importantly, I think the width of the moat is less relevant than whether the moat is widening or shrinking. Companies that successfully invest on widening their moat increase their durability.

Attractive price - It’s better to pay a fair price for a wonderful business than a wonderful price for a fair business. At the end of my analysis I usually build a valuation model and try to estimate the intrinsic value of the business. Nothing complex or fancy. The assumptions for the model are based on an analysis of the traits above. If the intrinsic value I estimate is lower than the current price, then I believe I’m getting close to a fair price.

As a reminder, before even looking at the characteristics above, I would filter the business depending on whether it’s within my circle of competence. If the company operates in an industry that I don’t understand I automatically discard it. Furthermore, I tend to exclude low-quality industries, such as airlines, commodities, and automotive manufacturers. I also have to say that there are some businesses that excel so much in some of the categories above that I’m willing to give them a pass on some of the others. Time will tell whether this is a good choice or if I should be better off being more rigid.

Valuation

What is smart at one price can be dumb at another, even when buying great companies. Waiting for a great business to become available at an attractive, or even fair, price requires patience and discipline.

I don’t anchor myself to basic pricing ratios, such as the P/E ratio. They tend to reflect the immediate past or the present, whereas all of the value of an investment lies in what will happen in the future. Us humans are terrible at forecasting in a non-linear way, which does not help our cause.

I focus on the following metrics when valuing a business:

Growth - future growth potential and, to a lesser degree, track record.

ROIC - returns on capital invested is one of the key value drivers for a business. It’s also important to keep track of a business’ returns on incremental capital invested.

Operating profitability - tells me a good bit about the fundamental strengths/weaknesses of the business.

Free cash flow - future free cash flow generation (per share!!!).

These are all related in some way. The first two are the main drivers of value creation, while the bottom two are the outputs I like to use to measure this value creation. My favorite valuation ratio is the free cash flow yield, because it tells me, as an owner of a business, how much cash flow I’m getting based on the price I’m paying. That said, what’s important is the future free cash flow generation, and many companies don’t optimize for it today.

![FCF Yield: Unlevered vs. Levered Formula and Calculator [Excel Template]](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Fae882f12-f566-4b2d-a07f-772ec56d79d4_1920x800.jpeg "FCF Yield: Unlevered vs. Levered Formula and Calculator [Excel Template]")

Inactivity and Patience as a Virtue

After finding a great business, run by good managers, at an attractive price, the best thing to do is: nothing. Too much activity can be the enemy of the great investor. Markets can be tempting with a myriad of “expert” opinions, commentary, short-term price fluctuations and what not. But if your analysis is correct, and the price you paid was prudent, sitting on your ass and reaping the benefits of business value creation is the soundest long-term approach. There’s no bigger mistake in investing than failing to allow your investments to compound by hopping in and out of positions. The financial services industry today is geared towards encouraging client activity. Strategic and tactical asset allocations, sector over/underweights, and macro forecasts are some common excuses that allow the industry to extract fees. Doing nothing helps you pay less in fees and commissions. Don’t fall for the promises of activity.

This doesn’t mean you should never sell. Ideally I would like to hold an investment forever, but realistically too many things change in business and life for that to be doable. I have 3 reasons that would lead me to sell an existing investment:

Realize and accept a mistake - this can be a mistake with the thesis or process. Maybe there’s a key factor I missed. If so, I evaluate and sell if necessary.

Competition for capital - in my case, if my portfolio is already at its maximum number of holdings (25), and I have a fantastic 26th idea, it’s worth considering whether the 25th best idea really belongs in the portfolio.

Change in outlook - when the thesis breaks. Perhaps management made a huge move that completely changes the business, or a new law affects the business in a meaningful way. Sometimes the business just deteriorates (but there are usually signs of this, so I if missed them it was probably a mistake on my end). Many things could cause an investment thesis to break. It’s important to recognize when that happens. One bad quarter doesn’t break a thesis.

Notice none of the three reasons have to do with price. The market will do what the market will do. I try to pay attention to what matters. If none of the three reasons above materializes, I do nothing.

Hope you enjoyed and gained at least some insights from reading about my investment strategy! The hardest thing is probably finding the balance between staying consistent while simultaneously identifying points for improvement. The above is what works for me, and I think it’s a must to find what works for you. I didn’t touch on sizing positions within the portfolio, but that can be a topic for another time! Make sure to subscribe and share if you enjoyed!