Moncler S.p.A. Investment Thesis

Moncler S.p.A. Investment Thesis

Plus: A Short Portfolio Update

Housekeeping

As a quick disclaimer, what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

I encourage you to do your own research on every potential investment. I’m comfortable with my portfolio, but none of my holdings are investment recommendations. I specifically talk about some buy/sell decisions below, so please don’t consider any of my comments as guidelines for your own portfolio.

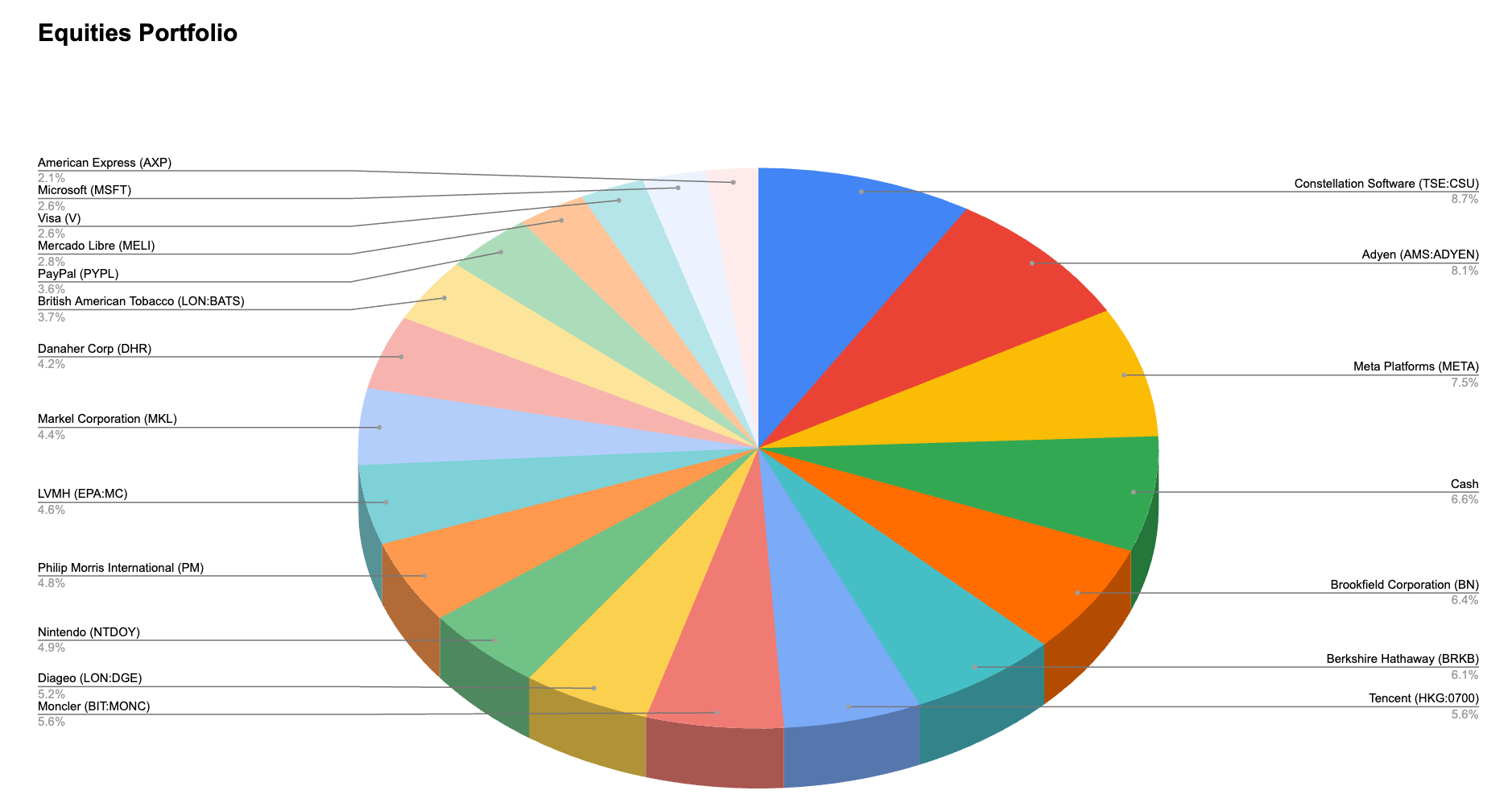

Portfolio Update

It’s been almost a year since my last portfolio update (link here), and I’ve made some recent moves that I thought warranted some comments. I consider myself a long-term investor, focused on the fundamentals of businesses rather than on trying to time the market, but 2023 seemed to be a more hectic year than I anticipated. I constantly put money into the portfolio though, and as you can see in last year’s breakdown, cash levels were elevated. So it’s not surprising to see a few new names. You can compare with last year to see the new positions, but right now I want to focus on three specific names: Tencent (HGK:0700), Alibaba (BABA), and JD.com (JD). The last two shine because of their absence in my portfolio today, even though I’ve written extensively about China, and I even made a case for investing in JD back in May of last year (link here).

The main reason I sold JD, and Alibaba, was that in late December Tencent stock took a beating due to a badly timed comment on tighter gaming restrictions by one of China’s regulators (those guys really didn’t get the memo - the comments were quickly rolled back). I’ve admired Tencent for quite some time. I believe that it enjoys the economic high ground in China’s technology ecosystem, and lacks the competitive pressures JD and Alibaba have to deal with in e-commerce. Tencent finally got to a valuation that met my return hurdle, so I swapped the positions to keep my China exposure consistent. I also sold Google in January, at a gain, so realizing the loss in JD/BABA helped me offset it and reduce my tax bill. Now I own a company like Tencent which, in my opinion, has a superior business model and management, and I was able to to purchase it at a very attractive price.

I felt that since I publicly wrote about JD.com as a good opportunity I needed to explain why I no longer own it. For the record, both the JD.com and Alibaba investments lost money, and my cost basis on Tencent is HKD 261.00.

Investment Thesis: Moncler SpA

The previous write-ups I’ve published on individual names have been in more of a long-form format. I wanted to try something different for this one.

Quick Introduction

Moncler SpA is an Italian luxury goods company, although it was originally founded in Monestier-de-Clermont, France in 1952. From its inception until 2003 it was mostly a producer and seller of winter jackets for workers and expeditioners. It was bought in 2003 by Italian businessman Remo Ruffini when the company was nearing bankruptcy. As CEO he succeeded in a remarkable turnaround, transforming Moncler into a luxury fashion house anchored around the puffy jacket. The company IPO’ed in the Milan Stock Exchange in 2013. In Dec 2020, they acquired Stone Island, an Italian luxury streetwear brand, and for the last 10 years Moncler itself has been expanding into new categories, such as skiwear, leather goods, and footwear. Today, as of Feb 2nd, 2024 the company has a market capitalization of EUR 15.44 billion or EUR 57.17 per share.

Below is a neat summary of Moncler’s revenues by brand and geography as of Q1 23, courtesy of Quartr:

Investment Case

Strong pricing power thanks to social-positional brand. Low cyclicality driven by wealthy clientele and true luxury demand, as opposed to aspirational luxury brands such as Gucci.

Returns on capital in the mid-to-low 20s, gross margins in the high 70s, and operating margins in the high 20s.

In the early stages of expansion to categories beyond winter apparel, such as shoes and leather goods. Both Asian and North American markets remain under-penetrated by Stone Island. This offers a strong runway for growth and reinvestment.

Clear strategy of channel optimization to reinforce exclusivity, increase the long-term value of the brands, and drive higher margins and returns on capital.

Conservatively financed company. Over 27x interest coverage and 0.4x Net Debt to EBITDA. Insulated against market downturns thanks to true luxury demand.

CEO, Remo Ruffini, owns ~23% of the company via his investment vehicle. Manager with skin in the game and experience leading the business through turbulent times, having executed one of the most phenomenal turnarounds in the luxury business.

Even though there’s been a recent bounce, the market has soured on luxury goods stocks due to a growth slowdown post the stimulus-driven acceleration of 20-21.

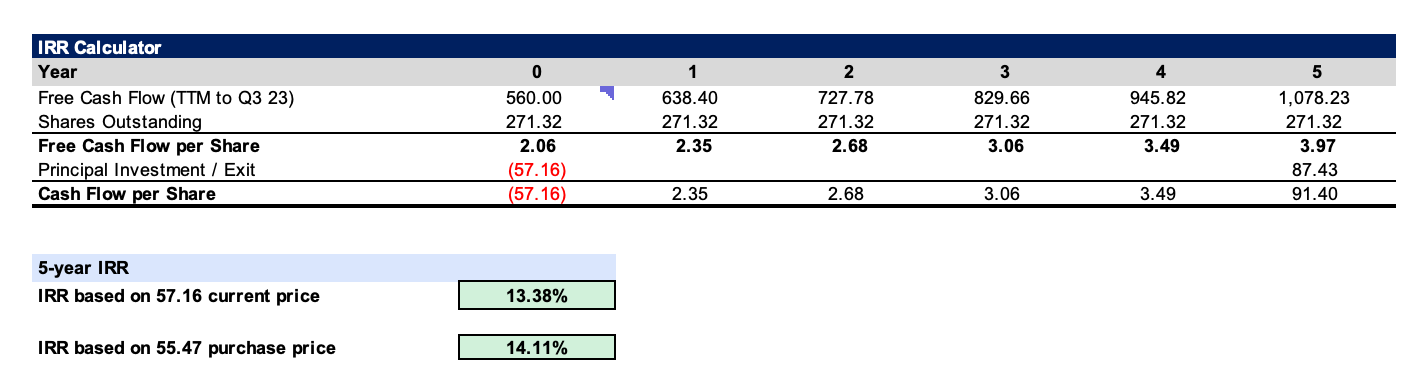

Valuation

With a 5-year horizon, assuming Free Cash Flow growth in the mid-teens level (compared to an almost 40% CAGR during 14-19), driven by pricing power, growth in newer categories, and Stone Island growth + channel optimization. No share buybacks. No multiple expansion, i.e., 22x FCF multiple.

With these relatively conservative assumptions, annualized returns come out at ~13%-14%* from today’s prices. Not bad for a business with strong growth tailwinds, high margins and returns on capital (and a clear path to expanding these), a conservative balance sheet, and a brilliant owner-manager.

Please do your own due diligence before making any investment!

That said, I hope you enjoyed this post! I think I’ll stay with these short-form theses in the future as 1) they’re less time-consuming, and 2) they’re more useful. Deep dives are interesting, but at the end of the day an investment thesis should be simple, clearly laid out, and actionable. I don’t foresee 2024 to be as hectic as 2023 and good ideas are rare, so don’t expect too many of these in the near-term! Thanks!