Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

As of the time of writing, I do not own shares in Markel, so don’t take what you read as investment advice or as an investment thesis. My goal with these posts is to further understand, and help others understand, how interesting companies operate. If they turn out to be good investment opportunities, that’s a plus. Always do your own research before making any decisions to buy or sell an investment.

Intro

“Tom, the secret of success in investing is lasting the first 30 years.”

Usually when someone says that “you should invest in such and such company because it’s the next X”, I believe that you’re usually better off just investing in “X”. So the first time I heard that Markel is sometimes referred to as the “Baby Berkshire”, my first instinct was to quickly dismiss it since I was already an investor in Berkshire Hathaway. Until I went on a binge of Tom Gayner podcast appearances. As of 2023, Tom is Markel’s sole CEO, having previously shared the position with Richard Whitt III since 2016. He is also Markel’s acting CIO, managing the company’s investment portfolio, where he has built an impressive (and deserved) reputation as a top capital allocator. Listening to people like Tom is a breath of fresh air for anyone interested in actually investing in businesses, rather than rolling dice. The power of good capital allocators often gets underestimated in the potential success of a business venture. But while Tom has been an integral part in getting Markel to where it is today, the company began operating long before.

Markel is also a lot more than simply an investment business. It’s a company with many moving pieces, so let’s get to it.

Brief History & Facts

Markel is actually a family business. It was founded in Norfolk, Virginia all the way back in 1930 by one Sam Markel, although at that time it was known as the Mutual Casualty Company. He started the business to insure jitney buses, and later began to selectively cover long-haul trucks, since traditional insurance carriers were not comfortable with them at the time. Markel has never been afraid to be contrarian. In 1935, Sam’s four sons joined the business and Markel Service Inc. was officially born. By 1940, American Fidelity & Casualty, a sister company, became the leader in covering fleets of trucks and buses. In 1951, the company expanded internationally for the first time, establishing a subsidiary in Toronto, Canada.

Markel Corporation was listed on the NASDAQ exchange in 1986, initially trading at a market capitalization of $15 million. After the IPO, the company began an active strategy of growth via acquisitions. From the 2002 letter to shareholders👇🏽

“Buying troubled <insurance> companies and fixing them has been our growth strategy.”

One of the most important acquisitions was that of Terra Nova Holdings in the year 2000, after which they opened an office in London. This gave them access to the international specialty & casualty market and effectively doubled the size of the firm’s insurance operations. Other notable insurance acquisitions along the way have been those of Essentia Insurance Company (2012), Alterra Capital Holdings (2013), SureTec Financial Corp (2017), State National Companies Inc (2017) and Nephila Capital Ltd (2018). Thanks to these acquisitions and contributions from organic growth, Markel wrote $9.8 billion in gross premium volume in 2022. According to NAIC, they’re the 23rd largest P&C insurer in the United States.

In 2005 they kicked-off Markel Ventures, not to be confused with a venture capital operation. Much like Berkshire Hathaway (the comparisons are not for nothing), Markel took advantage of the float from insurance operations and began buying entire businesses, bringing them under one umbrella. AMF Bakery Systems, a baking equipment manufacturer, became their first investee back in 2005. There are now 19 businesses within Markel Ventures. They’ve acquired more than 19, but grouped a few into what is now Markel Food Group.

While Markel was a family-run business for many years, there are no members of the family in the executive management team today. They have fully made the transition to “external” management. Tom Gayner, who as we mentioned has been in the company since 1990, is the current CEO. I wouldn’t exactly call him an outsider. Steven Markel and Anthony Markel, both members of the family, are in the Board of Directors however, with Steven being the Chairman of the Board. While Markel Corporation is now a large, diversified financial holding company, employing almost 21,000 people, they continue to live by what they call the Markel Style. Some highlights 👇🏽

“Our creed is honesty and fairness in all our dealings”

“<We> seek to be a market leader in all our products.”

“<We> seek to know our customers’ needs and to provide our customers with quality products and service.”

“Our pledge to our shareholders is that we will build the financial value of our company.”

“We respect our relationships with our suppliers and have a commitment to our communities.”

“Above all, we enjoy what we are doing.”

Tom Gayner speaks constantly about their Win-Win-Win culture, in which they seek to do business that results in wins for employees, for customers, and for shareholders.

Business Model: Markel’s 3 Engines

The simplest way to understand Markel’s business is to picture it as a vehicle with 3 distinct, but interconnected, engines: Insurance, Investments, and Markel Ventures.

Insurance - The Original Engine

Markel’s origins lie in insurance, and it remains an extremely important side of the company today. Insurance is a curious business. It’s extremely tough to build a competitive advantage because it is generally a commoditized product. If you’re searching for auto insurance, for example, policies tend to be very similar. In the end you’ll probably select the cheapest one available. It’s also an industry that’s heavily exposed to folly. The temptation to write more and more premiums without much regard to the risk being insured is often overwhelming. Consequently, competitive advantages in insurance can result from two sources: underwriting culture, and being a low-cost operator, which is in turn a derivative of culture.

Markel engages in 3 types of insurance activities:

Underwriting → focused on specialty insurance, which provides coverage for hard-to-place risks that generally do not fit the underwriting criteria of standard carriers. In other words, Markel likes to insure risk that standard insurance firms refuse to take on because of its complexity. This reduces competition in the form of pricing, which helps keep certain unwanted behaviors at bay.

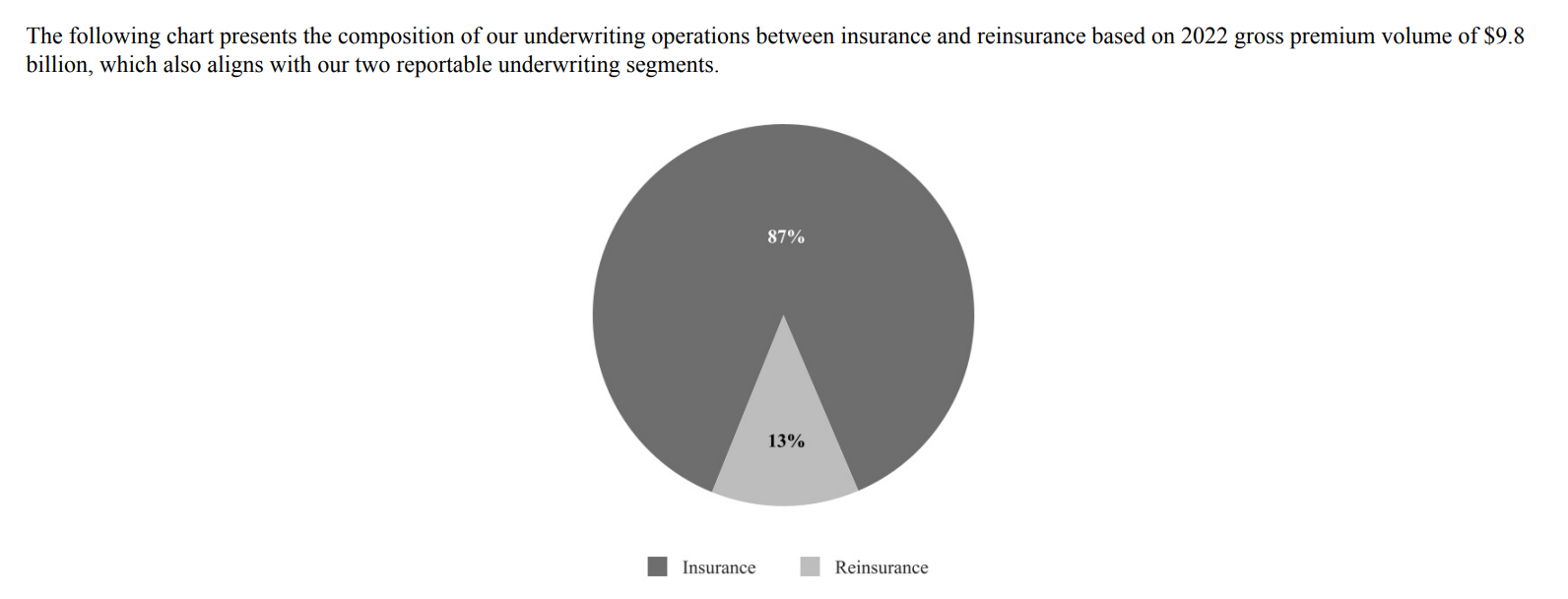

Underwriting activities are further sub-divided into insurance and reinsurance👇🏽

Insurance-linked Securities (“ILS”) → is a fairly new line of business, and is primarily comprised of the operations of Nephila Capital. Through this line of business, Markel essentially connects companies in need of reinsuring certain risks with 3rd party investors willing to put up a certain amount of capital to earn a return. Markel “packages” these securities and earns management fees based on the amount managed, as well as incentive compensation for achieving a certain level of returns on some funds. Think of this as Markel using the reinsurance market to provide an alternative asset class for large institutional investors.

Program Services and Other Fronting → through this business, Markel earns fee income in exchange for fronting insurance business to other carriers. Fronting refers to writing insurance on behalf of a client and then ceding (almost) all the risks to them in exchange of fees. The easiest way to understand this is to picture a small InsureTech startup that’s interested in writing policies, but lacks the appropriate license to do so. This startup could go to Markel and offer policies to clients piggybacking off of Markel’s permission to write insurance business. The startup gets the premiums less a “fronting fee” paid to Markel.

Zooming out a bit again, let’s focus on Markel’s underwriting operations for a minute or two. One important concept in insurance is that of float. Briefly, float is the money that an insurance company receives as premiums. Since claims are generally filed much later than when premiums are received (and not every customer ends up filing a claim), insurance companies can make a decent return by investing these monies in the meantime. Warren Buffet’s empire is built on float and investment acumen. It’s that powerful. Unfortunately very few insurance companies have the ability to make the most out of float. One of the great dangers in the insurance business is to seek premium growth at the expense of underwriting profits. Inadequate pricing will get an insurance company in trouble much faster than losing premium volume. This is why Markel’s approach is simple:

“The principles that support profitable underwriting are the same ones that lead us to superior investment results and, in turn, help us build shareholder value. These principles are: maintaining a long-term time horizon, discipline, and continuous learning.” - 2006 letter to shareholders.

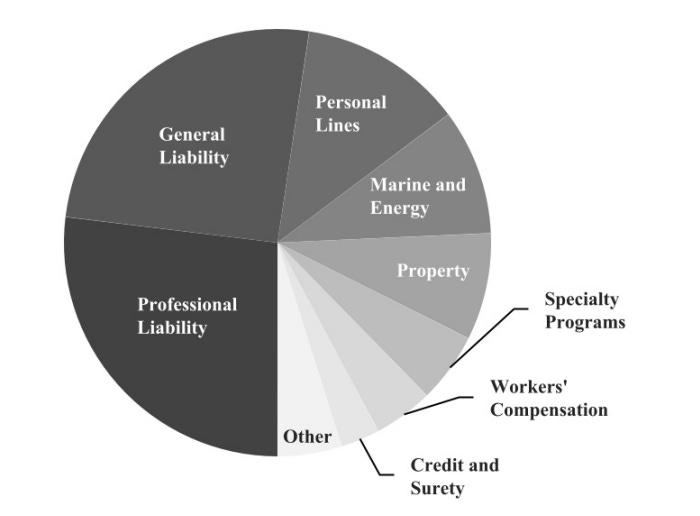

Their deep presence in specialty insurance, which is by definition less sensitive to price and more sensitive to availability, service, and expertise, is one way in which Markel gives itself an advantage. Below are the splits of Markel’s products by premium volumes in the insurance and reinsurance segments:

Markel also previously wrote property reinsurance and retrocessional reinsurance , but they discontinued writing new business in these lines because of the long-tail nature of these risks. There’s this famous saying about discovering who’s been swimming naked when the tide goes out. In insurance, the tide going out tends to take the form of years with a large number of severe natural catastrophes, such as 2005, 2011 and 2017. Markel has never been swimming naked, but by exiting business lines in which losses tend to be tough to bear they’ve put on a full wetsuit. Why take the chance, eh?

In another example of Markel’s conservatism, they’ve been consistent on their approach to reserving for losses. Their ultimate goal is to establish loss reserves that they do not have to increase in the future. They do this by operating with reserves levels that “are more likely to be redundant than deficient.” In other words, better to err on the side of caution.

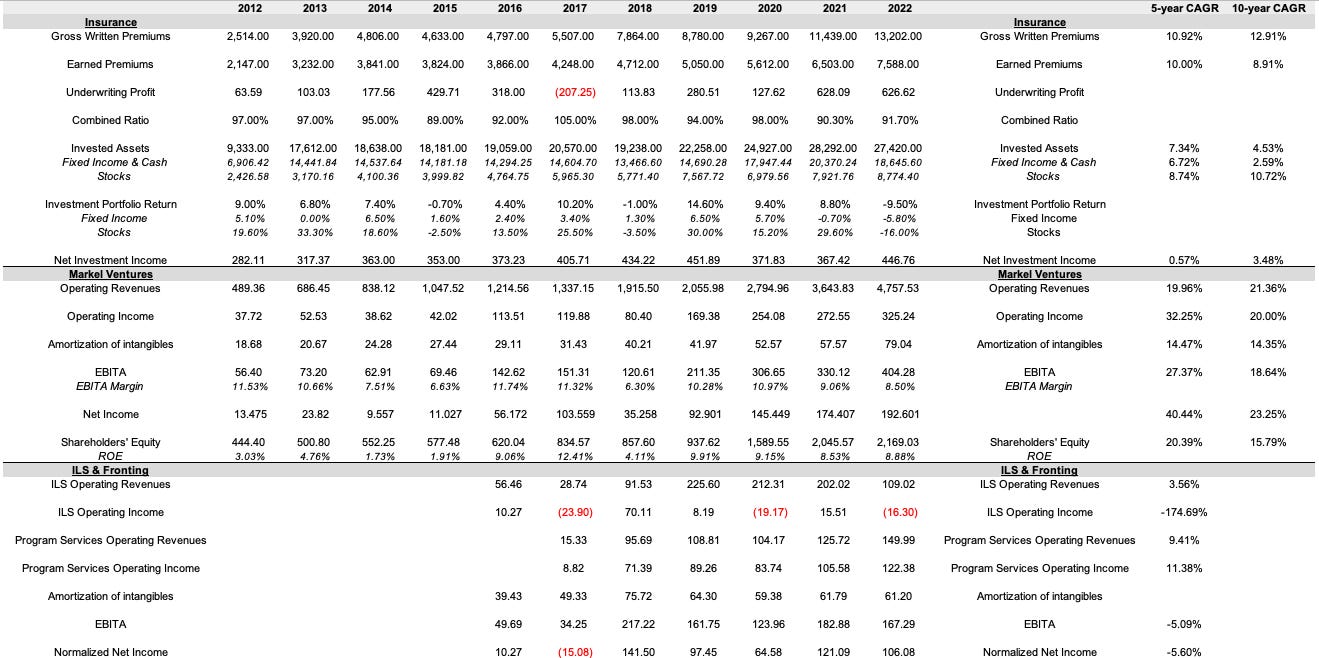

So, what does Markel have to show for their conservatism? Out of $13.2 in gross written premiums during 2022, $9.8 billion relate to their underwriting operations. This is up from $3.9 billion in 2013, for a CAGR of ~11%. Consistently throughout this period, Markel has been earning an underwriting profit and outperforming the rest of the industry👇🏽

The combined ratio is a key insurance metric that measures profitability. It accounts for both losses and operating expenses, and compares it against earned premiums (i.e., premiums were no losses will be paid out). Clearly, Markel has been doing alright when it comes to underwriting. Theres’s this curious fact about insurance, where living through different types of catastrophes and learning about them, and adjusting the way you approach certain risks, gives you a decisive advantage over those who either haven’t lived through enough of these events or just haven’t learned from them.

The story is a bit trickier with ILS. It’s been a bit of a mixed bag so far. In 2015, Markel acquired the assets of CATCo, a company that led the creation of insurance-linked securities. Unfortunately, during 2017-18 CATCo experienced severe losses due to record levels of property catastrophes. There was an inquiry into the setting of loss reserves at CATCo, and basically all of the capital invested in CATCo funds was tendered for redemption by investors. These operations were placed into run-off, meaning they are no longer doing new business. In March of 2022, Markel completed a buy-out transaction with CATCo in which they paid out $101.9 million to the benefit of investors in CATCo funds.

Currently, Markel is mainly operating in the ILS market through Nephila, which as mentioned above is essentially a fund management operation. So while Nephila is not taking the risk from reinsurance, it is still exposed to losses inasmuch as they result in lower performance for their funds. Bad performance means lower fees. It deters new capital from coming in and existing investors from renewing their existing deals. Performance in the ILS market has been impacted in the last few years due to elevated catastrophe losses. In 2022, Markel recognized a goodwill impairment of $80 million related to Nephila, reducing goodwill to ~$221 million. On the positive side, during 2022 Markel also sold the majority of its controlling interests in Velocity and Volante for a cumulative gain of $226 million, two operations that were part of their Nephila acquisition. Velocity provides risk origination services for Nephila’s fund management business, and Volante underwrites and administers specialty insurance and reinsurance policies and provides delegated underwriting services to 3rd party investors. Markel did this to unlock the value created in this two operations since 2018, as well as to concentrate its efforts in Nephila’s core fund management business. As of 2022, the ILS business is doing less than half the revenues it did during 2019, and still posting operating losses. While Markel is adamant on the future potential of the ILS business, it remains a small part of the company so far.

Finally, Markel offers its Program Services through State National. They wrote gross premiums of $2.8 billion during 2022, up from $2.3 billion in 2019. Markel reinsures practically all of the risks inherent in their program business, but they’re still exposed to a portion of the underwriting risk here.

Investments - The Secret Sauce

The 2nd of Markel’s engines is its large investment portfolio. As of December of 2022, total invested assets equalled $27.4 billion. That’s a lot of dough. The majority of these funds come from the premiums paid by policyholders (“policyholders funds”). Markel invests these funds mostly into high-quality government and municipal bonds, as well as in shorter-term cash equivalents. They make sure that the currency and duration of these assets matches closely with the expected losses to be paid out to policyholders. Because of this they hold these assets to maturity, collecting income until they do, instead of buying and selling hoping for an increase in price. They do this because they cannot afford to not pay out claims to their customers. This is why the philosophy around loss reserves is also so important. If you don’t estimate losses from claims conservatively, there’s a higher likelihood that you’ll be caught out without enough capital to pay them out.

28% of Markel’s invested assets (approx. $7.6 billion), which is the excess over premiums paid by policyholders, is invested in stocks. This excess cash is the one Markel generates on its operations above & beyond what it expects to pay to policyholders. They’re able to do this because they have more surplus capital than they need to maintain a stable financial position. All 17 of Markel’s rated insurance subsidiaries have been assigned a Financial Stability Rating (“FSR”) of A, which translates to excellent. Without a strong emphasis on underwriting profitability and conservative reserving, Markel would not be able to invest a sizable amount of money into stocks and generate additional value in the form of a good return on their capital.

Tom Gayner highlights the 4 key characteristics he looks for in a good investment:

A profitable business with good returns on capital and low leverage;

Managed by a team with equal measures of talent and integrity;

That enjoys high opportunities for reinvestment and capital discipline; and

Trading at a reasonable price.

Simple. Elegant. Even though they own over 100 stocks, the portfolio is fairly concentrated, with the top 10 representing over 40% of the assets. Here’s how the portfolio looks like as of December 2022:

While many insurance companies invest their capital by allocating investments with external managers, such as hedge funds, private equity funds, and/or other alternative investment managers, Markel manages all of its investments in-house. This has one key advantage: cost. In the 2012 letter to shareholders, they revealed that the internal costs to manage their investments amounts to less than 10 basis points (0.10%) of AUM. Compare that with the 2 & 20 arrangement they would be paying an external manager.

The equity portion of Markel’s portfolio has returned 11% p.a. over the past 20 years. This compares to 8.1% for the S&P 500 over the same period (up to Dec 2022), including dividends. In fact, Markel has beat the S&P 500 over the last 5, 10, and 20 years. Way to go Tom.

Naturally, the total portfolio has returned a lower annual amount of 5.5% since the majority tends to be allocated towards fixed income and cash equivalents.

Markel Ventures - Cash Flow, Cash Flow, Cash Flow

“Markel Ventures does two things for Markel. One, it gives us another option for capital allocation decisions. Secondly, it makes a bunch of money.” - 2014 letter to shareholders

Even though the name might confuse some people, Markel Ventures is not a venture capital arm. There’s a reason why Markel gets compared to Berkshire Hathaway. All insurance companies produce float and invest it into bonds and (some) stocks. Some invest much better than others, but they all do it. But Berkshire Hathaway pioneered (I think, I haven’t verified this) the activity of buying controlling stakes in businesses using insurance float. These businesses generate cash flows, which combined with float can be used to buy more businesses, and on, and on, and on.

As the quote in the beginning of this section mentions, Markel Ventures is all about providing Markel with more opportunities to earn good returns on their capital. They apply the same 4 rules they use when looking for listed equities: profitable (non-insurance) businesses with good returns on capital and low leverage, managed by a team with equal measures of talent and integrity, with high reinvestment opportunities, at a reasonable price.

Similar to Berkshire, Markel allows the management of their portfolio companies to continue running their businesses, and it tends to stay out of their way unless there’s something that needs fixing. These businesses operate independently, with Markel’s management handling only capital allocation and reinvestment decisions. This differs from Markel’s approach to insurance acquisitions, where they’re very hands-on and rely a lot on their ability to right-size the culture and operations of these companies.

Another important note is that Markel doesn’t buy these businesses with the intention of selling them later for a meager gain. They’re in it for the long-haul, which is one of their main selling points as a potential acquirer, much like Berkshire Hathaway. This strong reputation as a long-term owner tends to attract owners who care deeply about their businesses, instead of attracting grifters who want to sell for a quick gain.

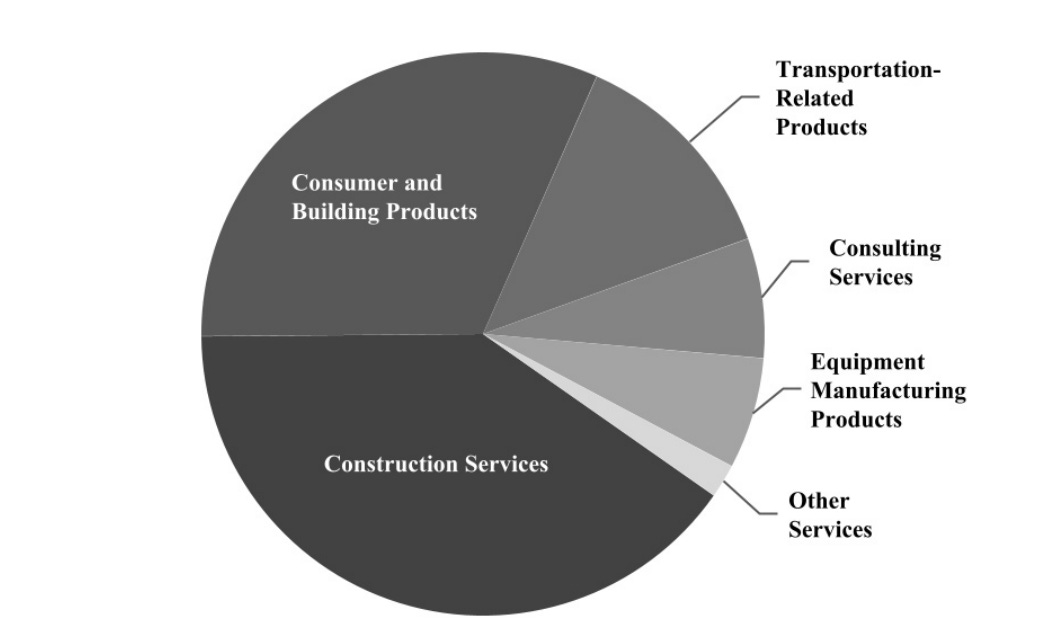

The types of businesses within Markel Ventures range from bakery equipment (AMF Bakery Systems), all the way through leather products (Brahmin), and to houseplants (Costa Farms). However, there is quite a large exposure to businesses involved in the housing and construction sectors, such as Buckner (heavy-lift cranes), Eagle (homebuilding), Metromont (precast concrete), Lansing Building Products (duh), VSC Fire & Security (installation of fire & safety systems), and Panel Specialists (interior design panels). As of 2022, Markel Ventures generated $4.76 billion in operating revenues, out of which 70% were related to consumer & building products and construction services.

These businesses are all headquartered in America, and generate 96% of their revenues from the US. Markel Ventures is a firm bet on the future of the USA.

Since 2005, when Markel Ventures started, Markel has cumulatively spent $3.4 billion to acquire all of these businesses, and they’ve built up cash balances of around $1.5 billion (these numbers are from 2021, but they made no new acquisitions in 2022). So the net investment is ~$1.9 billion. During 2022, they generated ~$400 million in EBITA, for a respectable return on capital of ~21%.

Financial Analysis

Summary

Below is a summarized version of Markel’s performance during the past decade:

Markel’s growth as a businesses can be visualized by comparing the two latest 5-year periods (2013-2017 vs 2018-2022). Markel generated:

$23.66 billions in gross premiums from 2013 to 2017 vs $50.55 billion from 2018 to 2022.

$19.01 billion in earned premiums vs $29.46 billion.

$821 million in underwriting profits vs $1.78 billion.

$1.81 billion in net investment income vs $2.07 billion.

$5.12 billion in Markel Ventures operating revenues vs $15.17 billion.

$500 million in Markel Ventures EBITA vs $1.37 billion.

$85 million in ILS revenues (only for 2016 and 2017) vs $840 million.

$15.33 million in Program Services revenues (in 2017) vs $584 million in the subsequent 5 years.

Apart from the mild growth in net investment income, which is also highly driven by a decade of persistently low interest rates, growth elsewhere has been quite solid.

Markel hasn’t posted an underwriting loss since 2017, once of the worst catastrophe years for the industry in terms of losses in history. The combined ratio for the past 5 years has averaged 94.40%. Good, but not exceptional. However, results during 2021 and 2022 were much improved, coming in at a combined ratio of 90.3% and 91.7% respectively. One aspect of Markel’s insurance discipline that is worth highlighting is that they don’t hesitate to scale back on growth if they see the market getting ahead of itself in regards to pricing, such as in 2015-16.

The growth in Markel Ventures has been explosive, with operating revenues growing at a 21.36% CAGR during the past 10 years. Growth over the past 5 years has been similarly impressive at close to a 20% CAGR. Net income has grown from $35.26 million in 2018 to $192.60 million in 2022. Throughout this time, the Markel Ventures operations have averaged an ROE of 8.12%.

While ILS operations have been a bit disappointing (revenues have dropped every single year since 2019), Program Services have been chugging along nicely, growing revenues at a 9.41% CAGR in the past 5 years. Combined, these operations generate ~$160-180 million in EBITA each year, ~$105-120 million in normalized net profits, and should continue growing at a moderate clip. I’m not too hot on the ILS business, but perhaps the renewed focus from selling the Velocity and Volante stakes will help improve performance.

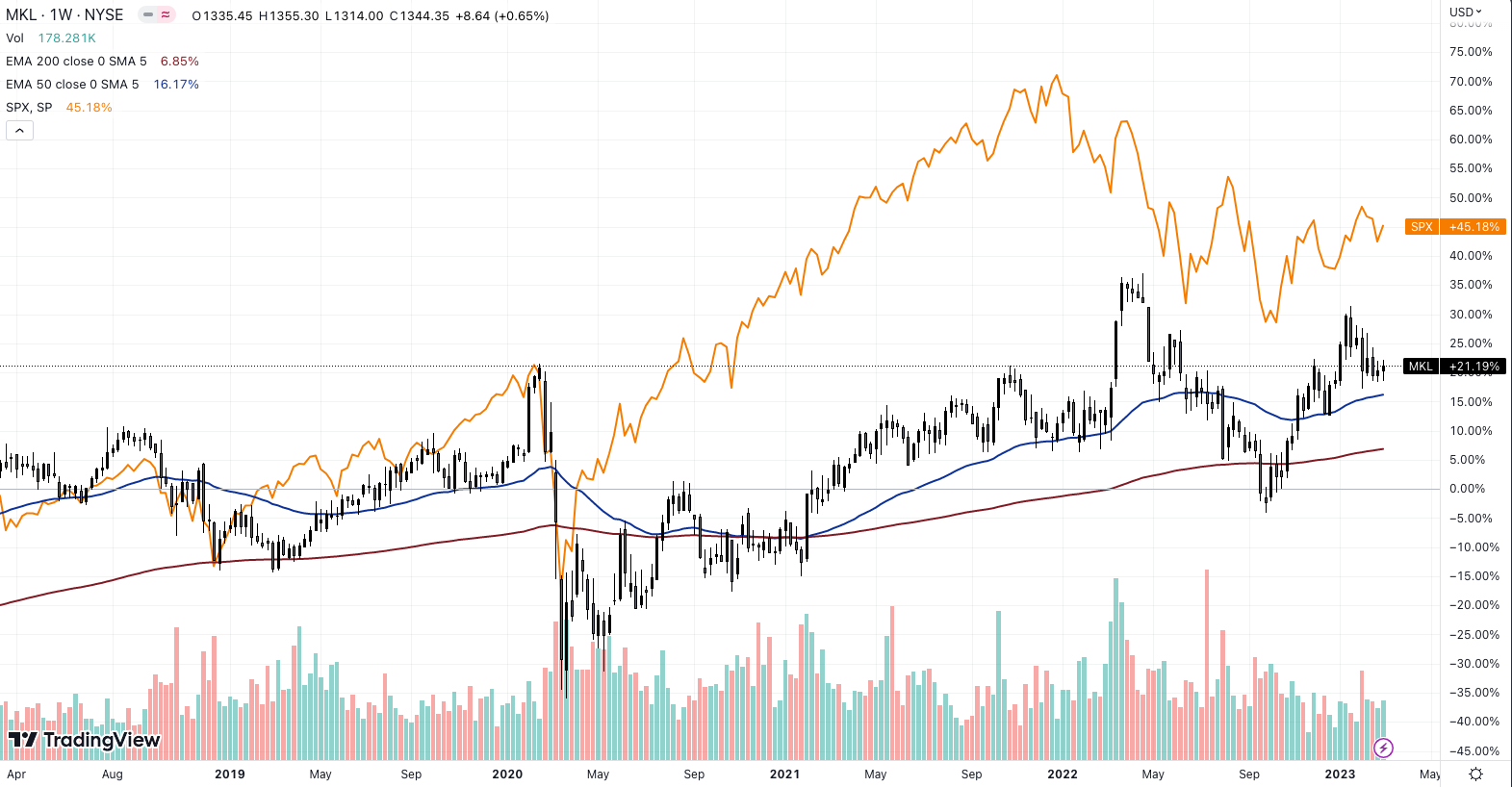

In regards to book value per share, which Markel looks at on a 5-year rolling basis to determine executive compensation alongside total shareholder return, results haven’t been so hot, growing only 7.28% p.a. since 2018. The stock has underperformed this book value growth, having compounded at a disappointing rate of 4.88% p.a. since 2018. Markel stock has decisively underperformed the S&P 500 during the past 5 years to March 3rd, 2023:

Capital Allocation

Markel highlights their priorities for capital allocation as:

Reinvest in organic opportunities in insurance or Markel Ventures. They always prefer to invest in their own people first, considering that they know what they’re capable of and the returns they can generate.

Acquire additional insurance businesses. They then apply their hands-on playbook of adjusting the underwriting culture to Markel’s, improving efficiency and revealing synergies between the new operations and existing insurance operations.

Acquire partial or controlling stakes in private or public businesses through Markel Ventures or their own investment operations.

Repurchase stock when there is excess capital and prices are favorable.

On any given year they could do all 4 of these. On the last point, Markel doesn’t have a programmatic approach to buybacks, instead preferring to be opportunistic. It’s clear that as their stock has lagged the market they’ve seen opportunities in amping up buybacks (negative in the chart represents more cash outflows to repurchase shares).

Compare that with where the stock has trade on a price-to-book basis for the past 2 years:

It’s worth mentioning that in 2020 (in May of 2020, to be more precise), they stopped repurchasing shares and issued $600 million in preferred stock close to the depths of the Covid market crash. In the surface, this looks like a terrible decision, but I think it speaks more of the inherent risks in the insurance industry than of the team’s capital allocation skills. We all know what happened with hindsight, but at the time I can see how the 2nd half of 2020 and beyond appeared to be uncertain. Their explanation, from the 2020 letter to shareholders makes a ton of sense to me:

“We made that decision to first protect the company in the face of such uncertainty and in order to maximize our ability to continue to write insurance premiums at favorable rates.”

In investing, standing ready to buy when everyone is running for the door is a huge strength. But if everyone is running for the door because of an event that could meaningfully affect the financial position of your business, I understand why you would not like to take chances. Also, based on the interviews I’ve listened to, Markel executives tend to emphasize the importance of doing right by their customers. In insurance, compromising your capital position puts you at risk of not being able to fulfill your promises to clients.

Finally on capital allocation, Markel doesn’t pay a regular dividend. It only pays a preferred dividend, which amounted to $36 million in 2021, and the same amount in 2022.

Valuation

In order to estimate an approximate value for Markel, I decided to try a reverse approach, first estimating the value of Markel Ventures and subtracting it from the current market cap to understand how the market might be valuing Markel’s insurance operations.

I applied an 18x multiple to Markel Ventures’ 2022 earnings of $192.6 million, close to the current market P/E (the S&P500 P/E is around 18x-19x at the moment). Even though this might seem a bit aggressive, I expect Markel Ventures to continue growing at a rapid pace and the increase in cash flows to result in opportunities to reinvest at high rates of return. Based on this estimate, the value of Markel Ventures is somewhere close to $3.5 billion, or 1.6x book value. I don’t think this is too aggressive. Consider that Markel has cumulatively spent $3.4 billion to acquire this group of companies.

Anyway, based on Markel’s current market cap of ~$18 billion, this means that the rest of Markel’s businesses are valued at ~$14.6 billion. This includes ILS & Program Services and the 23% stake in Hagerty, a publicly-traded specialty auto and boat insurer. Applying an 8x multiple to ILS & Program Services net profits of $106 million in 2022 adds up to ~$850 million in value for these business lines. Assuming Hagerty’s current market capitalization of $3 billion is the right value for the company (no strong opinion here) the additional $700 million in value from the stake means the implied value of Markel’s insurance operations is close to ~$13 billion.

For $13 billion, you can get an insurance operation generating close to $260 million in normalized underwriting profits, as well as a $27.4 billion investment portfolio generating close to $400 million in net investment income annually from interest and dividends . Out of this $27.4 billion, $8.77 billion are shareholders’ funds. This portion, which we can relatively accurately conclude is invested in the common stock portfolio, will probably compound at 8%-10% assuming Tom Gayner doesn’t call it quits.

The implied Price-to-Book of Markel’s businesses ex. Markel Ventures is ~1.04x. Look, this is not a clean valuation exercise by any means, but I prefer to be approximately correct than precisely wrong.

Risks

Ok, first I have to be a bit pedantic here and clarify what I think is not a risk here. And that is, alignment with shareholders. It’s pretty clear that, while they might not always make the correct decisions, Markel’s top brass is not only sharp, but also extremely aligned and committed to shareholders, employees, and customers. They won’t screw any of the stakeholders, and that goes a long way.

Some risks I do think are important to consider:

Catastrophe losses —> one of the main reasons that can lead to underwriting losses and low returns on capital. It also reduces the attractiveness of ILS products. A string of years with abnormally high levels of catastrophic events could result in a significant reduction of Markel’s value. That said, they have taken active measures to reduce exposure.

Under-reserving —> if Markel gets a bit loosey-goosey with their philosophy for loss reserves, or if they simply get it wrong, then earnings could suffer materially in the future. There is also greater uncertainty in estimating losses for long-tail coverages. I think Markel’s conservative culture will help them continue operating responsibly in this area.

Cyclicality —> the property & casualty insurance is highly cyclical, with periods of excess underwriting capacity that bring prices down and make writing business unattractive in terms of profitability. Markel has shown restraint before by prioritizing profitability before anything else.

Concentration —> the top 3 brokers that bring business to Markel’s insurance operations is close to 28%. Straining those relationships could hurt the business. I don’t see any reason why Markel would want to shoot itself on the foot though.

Acquisitions —> both with insurance and non-insurance operations, Markel has historically grown a lot by acquiring other businesses. Most large acquisitions tend to offer poor returns, so the risks inherent to acquisitions (overpaying, integration, lack of synergies, etc.) come into play here. Markel’s track record so far is solid, but it’s worth keeping an eye on their future acquisitions.

Conclusion

Insurance is one tough business. But if I were to look at what an insurance company could do to give itself an edge, it would be what Markel has done. Focus on underwriting profits, don’t be afraid to get your foot off the pedal when market conditions are not quite right, and conservatively reserve for losses. Prioritize the health of the balance sheet above all else, and take care of your customer. Invest in a sensible manner, staying away from the hype and remaining disciplined. Keep your eye on the long-term outcome. Finally, leverage your cash flows to generate more cash flows, diversify away from insurance, and remain focused on smart capital allocation decisions. Swim against the current, if and when you have to.

I was gladly impressed by Markel’s business, and will probably scoop up some shares now that the price is quite attractive. I do not think it’s going to be a ten-bagger anytime soon, but slow and steady wins the race. I hope.

Below are some incredible resources for you to learn more about Markel and Tom Gayner:

Richard Whitt (Markel’s former co-CEO) on the 2022 market outlook

Lovely article that analyses Markel as a potential acquisition for Berkshire Hathaway

Sweet and short Seeking Alpha article on calculating the mathematical value of Markel

Thank you so much for reading! Hope it was useful! Please do your own due diligence when considering a potential investment!