Just Another Goddamn Retailer

Just Another Goddamn Retailer

JD.com and the China Discount

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

It’s worth mentioning that I own shares in JD, so my opinion is not exactly free of bias. While I do try to look at investment opportunities as objectively as I can, keep that fact in the back of your mind as your read. This is not a deep dive or in-depth thesis. This is a brief summary of why I think JD looks like a solid investment opportunity at current prices.

Intro

JD.com (“JD”) is a Chinese online retailer / integrated supply chain services provider. It was founded in 1998 by Richard Liu as a traditional retailer. After the SARS epidemic struck China in 2003 JD pivoted towards online retailing. Today it is one of China’s largest companies by revenues, reaching over $150 billion during 2022. It is also within the top 30 Chinese companies by market capitalization at ~$55 billion as of May 12th, 2023. It trades in both the Nasdaq (ADR) and the main board of the Hong Kong Stock Exchange, and it’s a constituent of the Nasdaq 100. Even though Richard Liu stepped down as CEO in March 2022, he remains involved as Chairman of the Board and still owns a sizable stake of more than 12% of the company. Through his class B shareholding he also controls over 70% of the voting rights.

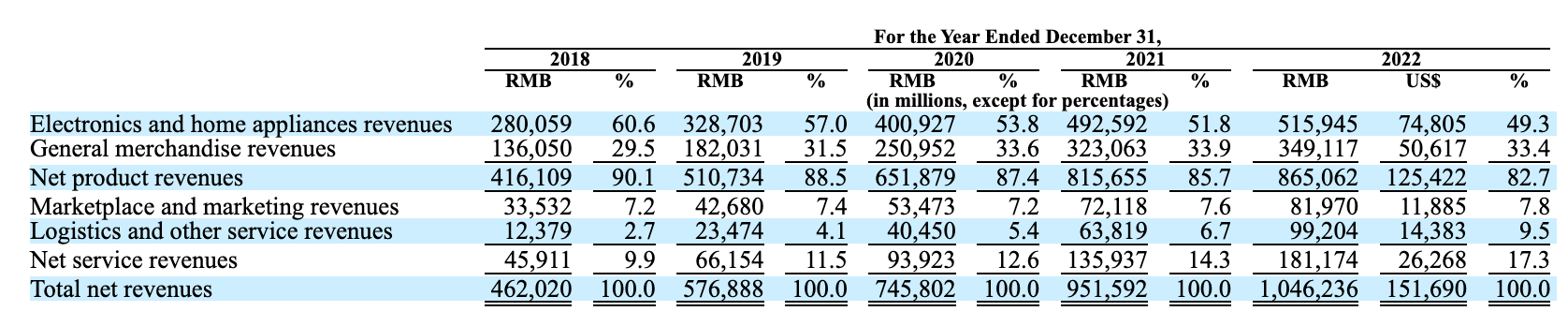

JD has historically focused on a 1P e-commerce model. This model resembles traditional retailing as JD purchases items from suppliers, which they then resell to customers for a mark-up. JD’s product sales have been concentrated in electronics and home appliances, which tend to be more discretionary. There’s still a considerable degree of concentration in this business line, representing over 80% of total net revenues. See breakdown below👇🏽

Since the early 2010s however, JD has also been operating its own marketplace, where 3P merchants can list their products for consumers to buy. JD also offers advertising & marketing services to these merchants. Naturally, these revenue sources come with much higher margins as they don’t require the procurement and purchase of physical items.

In its mission to provide exceptional value and a top notch experience to customers, JD has invested heavily in building out China’s most extensive logistics infrastructure. This allows the company to deliver products cheaply and quickly, almost anywhere in the country. They initially utilized this logistics network solely for internal purposes, but since 2017 they broke JD Logistics out into its own segment offering “a full spectrum of supply chain solutions and high-quality logistics services enabled by technology, ranging from warehousing to distribution, spanning across manufacturing to end-customers, covering regular and specialized items.” As you can see in the table above, “Logistics and other services” revenues, which consist mostly of logistics services offered to 3rd parties, have been growing at a rapid pace during the past few years.

Apart from these main business lines, JD also operates other smaller businesses. These include Dada, a local on-demand delivery and retail platform in China, JD Property, an infrastructure-focused asset management business, and JD Industrials, a supply chain technology and service provider. We didn’t even mention JD Health, an online healthcare platform, with its operations reported within the retail segment.

What happened

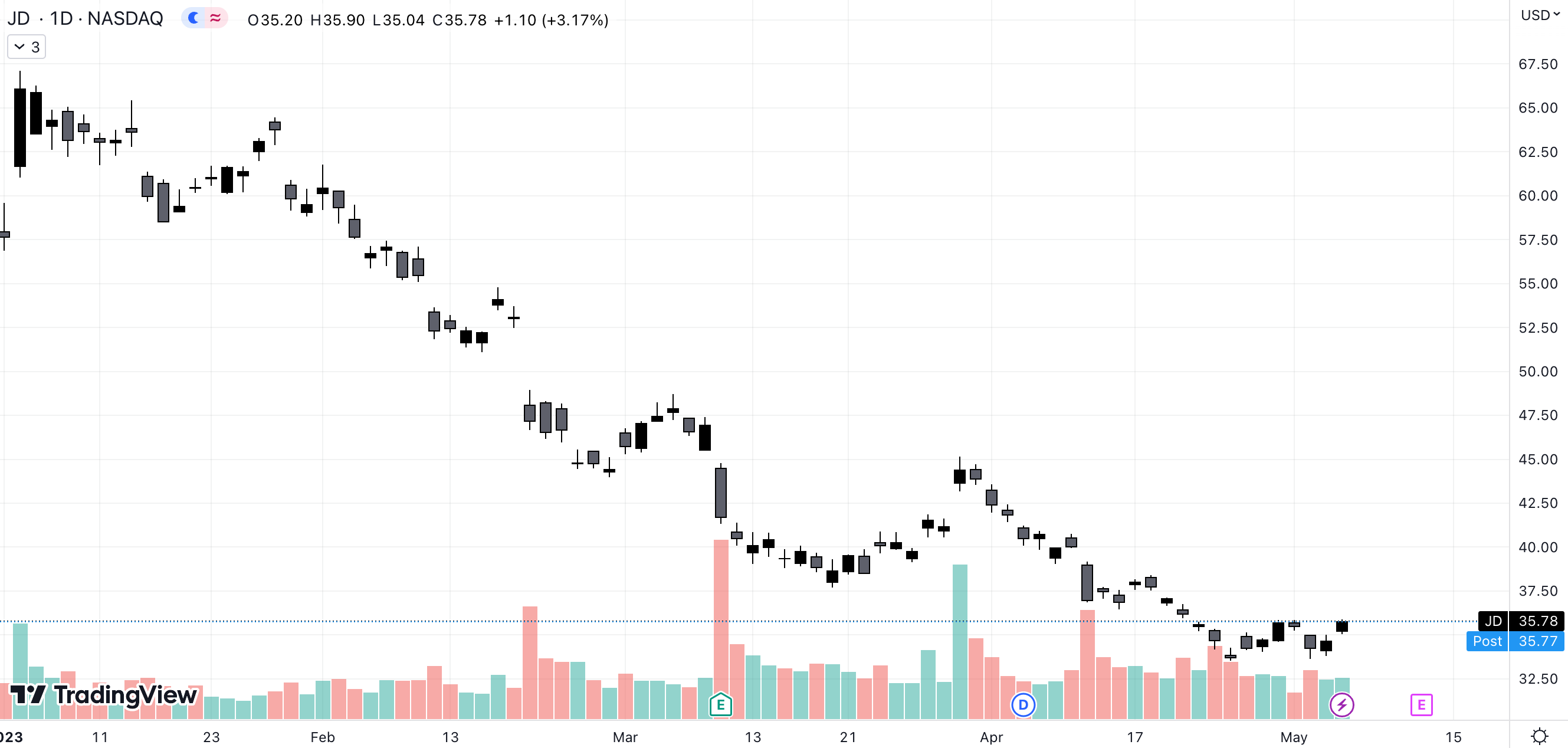

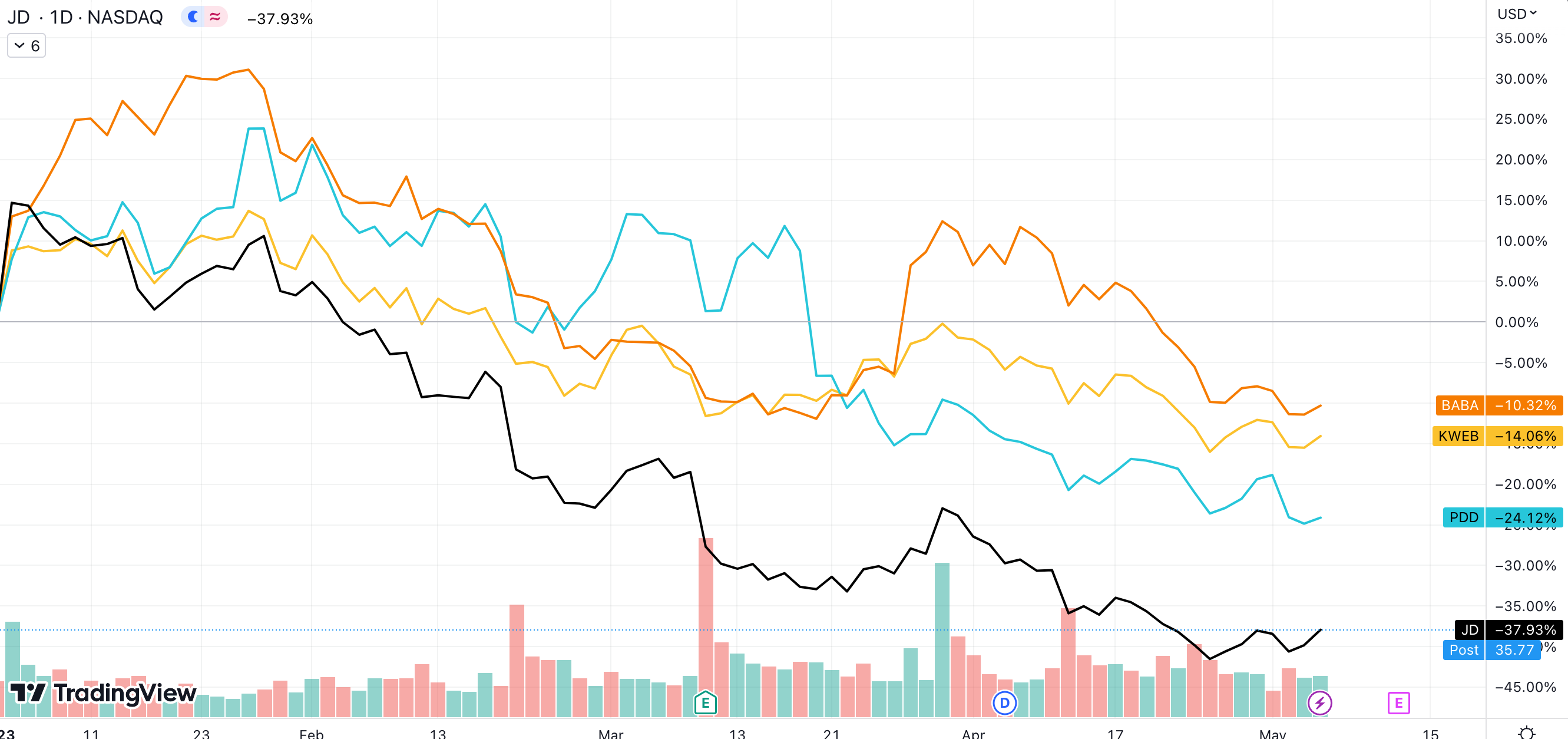

JD stock has taken a beating. Not only is it down over 40% since the start of 2023, it is also down over 65% since its peak above $106 in February of 2021.

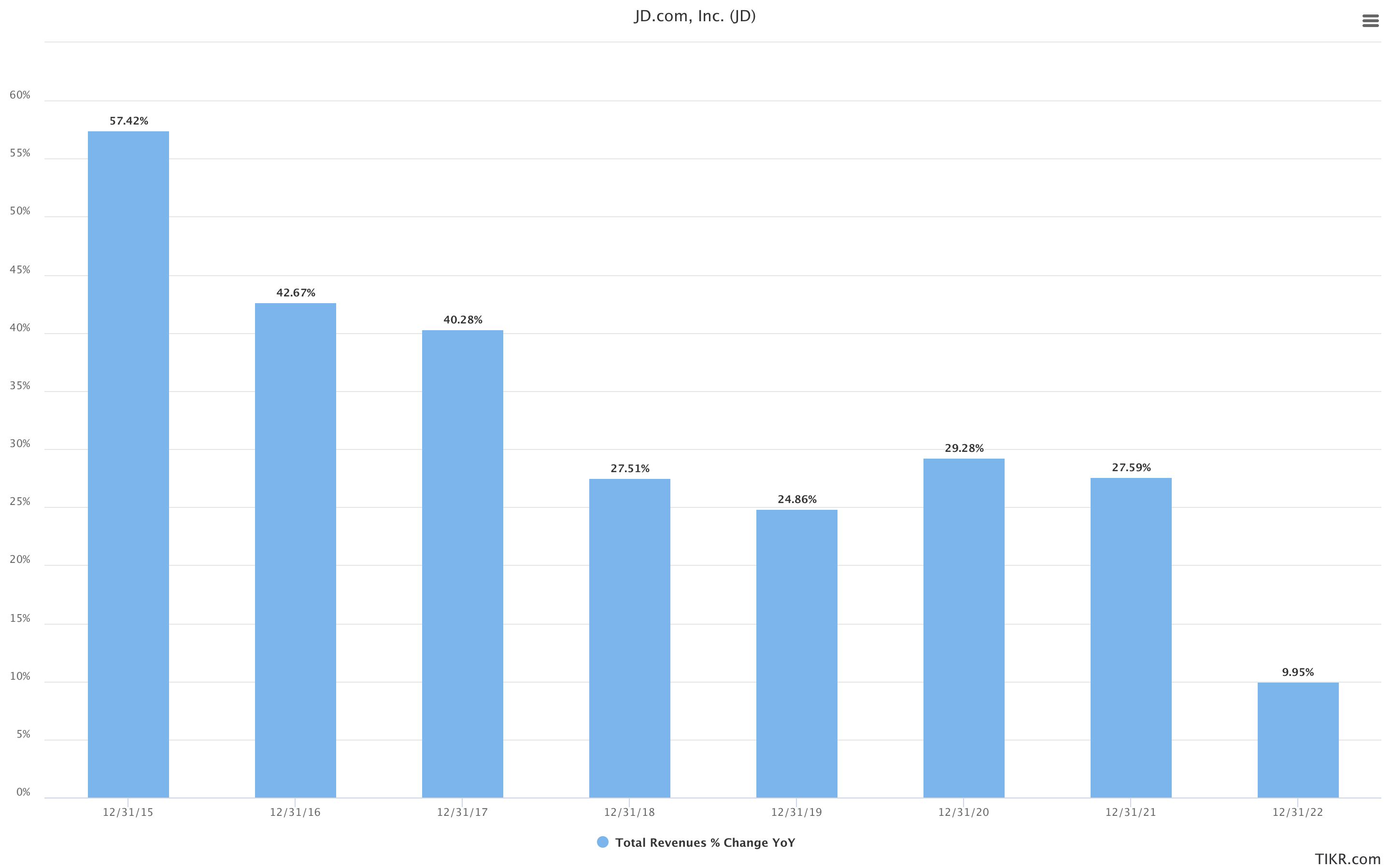

We know most of this story: Chinese tech stocks have been taken to the woodshed multiple times. Draconian Covid restrictions, regulatory crackdowns, a property bubble deflation, delisting concerns, and geopolitical fears are only some of the reasons. While Chinese tech stocks haven’t had the brightest start to the year, JD has noticeably underperformed its peers👇🏽

Why? It seems to be a mix of concern about:

Slowing growth —> Net revenues grew 9.9% during 2022, a considerable slowdown from previous years. Net product revenues grew only 6.1% year-over-year, compared to 25.1% year-over-year growth from 2020 to 2021. During Q1 23, growth was even lower. Net revenues grew only ~1% YoY, while net product revenues actually contracted. As mentioned before, JD’s product revenues are weighted towards appliances and electronics, which tend to be more cyclical than groceries, for example, for obvious reasons.

Price war fears —> In March 2023, JD announced a $1.4 billion “subsidy program” for merchants to provide discounts for consumers. Fearing a price war that would eat into profits, investors were concerned. One of JD’s main goals has been to attract more 3P merchants to their platform.

Why JD looks attractive at these levels

Growth re-acceleration

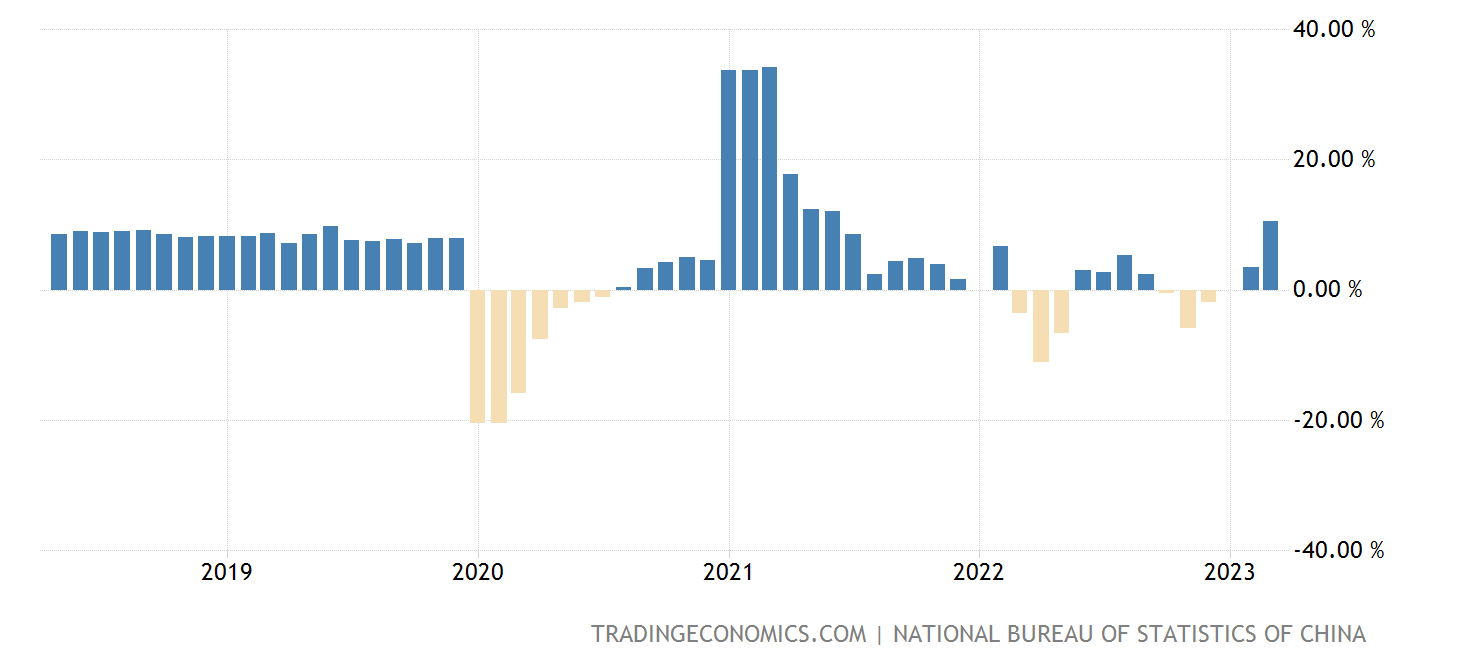

While growth has been slowing for some time already due to the much larger revenue base, 2022’s sharper slowdown was the result of macroeconomic pressures on the Chinese consumer.

Covid lockdowns were still a thing in China throughout 2022, which combined with the housing market slump resulted in a poor environment for consumption. Retail sales paint a clear picture of the deterioration👇🏽

The growth numbers posted by JD in such an environment are nothing short of impressive. Granted, there was an obvious boost from the Covid e-commerce bump. Still, as the Chinese economy reopens, the environment will eventually normalize and consumer confidence will most likely recover. Sandy Xu, current CFO and future CEO, highlighted Q2 23 is already looking much more encouraging👇🏽

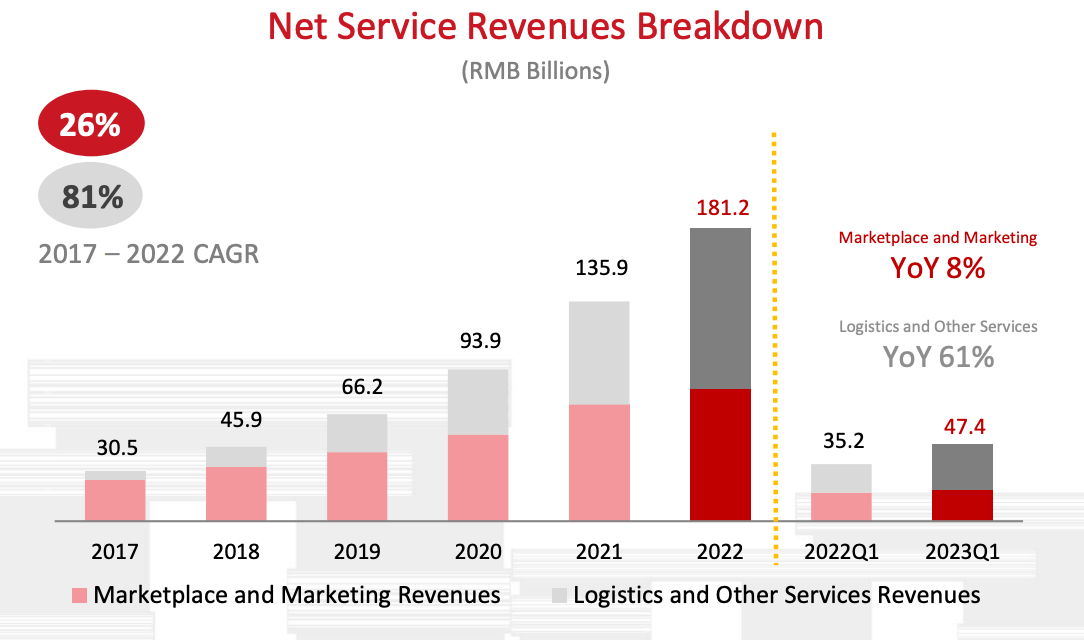

In the meantime, JD’s net service revenues continue chugging along nicely even during this tough environment.

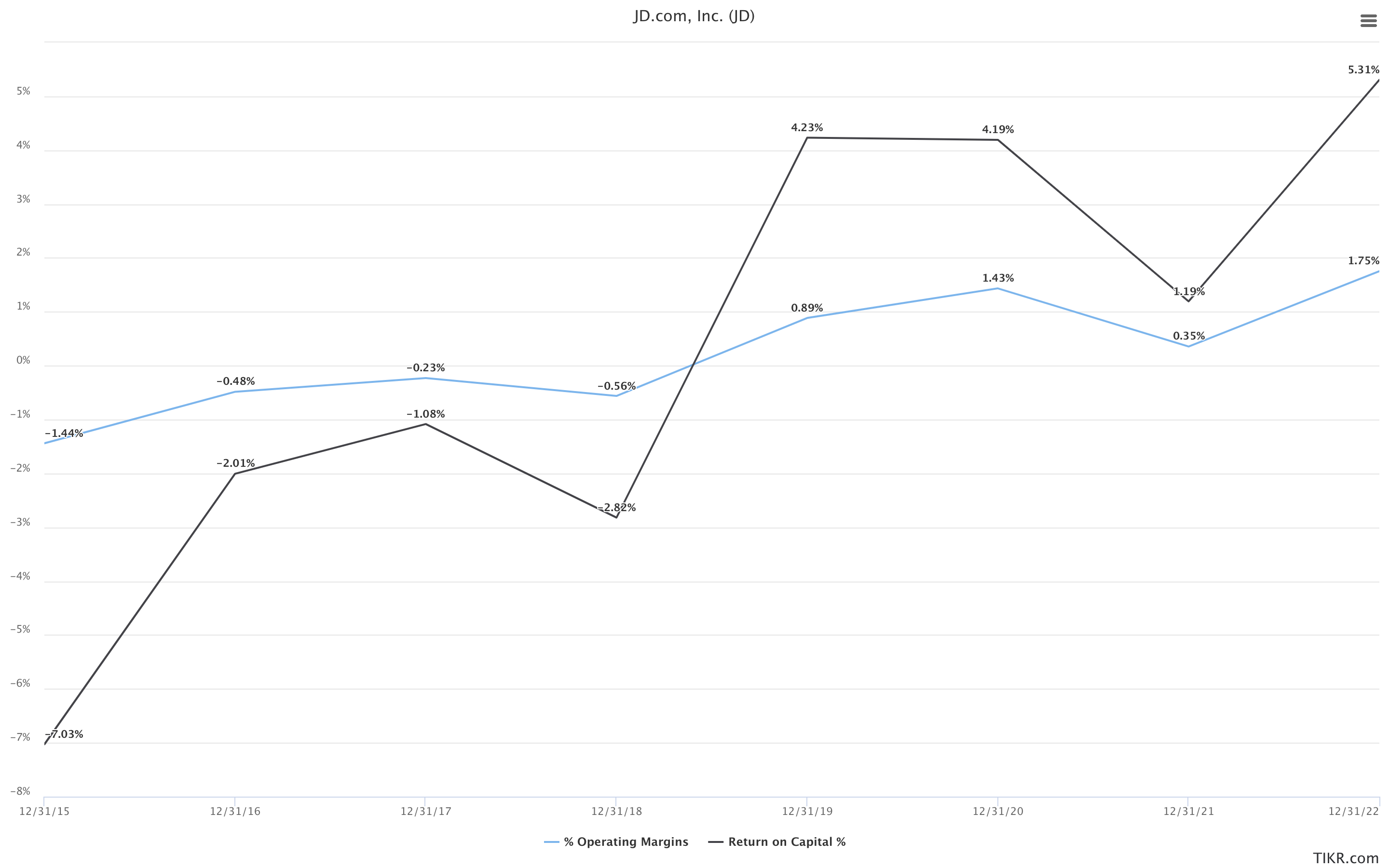

Margin Expansion and ROIC

An important growth lever will be the increase in higher-margin net service revenues, which includes marketplace, online marketing and logistics services.

The company will continue seeing benefits from its paid membership program, JD Plus, which currently boasts 35 million members as of Q1 23. JD Plus customers spend on average 8.4x what a regular JD user spends, while providing the company with a high-margin recurring revenue base. This is still at a small scale however, so there’s plenty of room to capture more paid members.

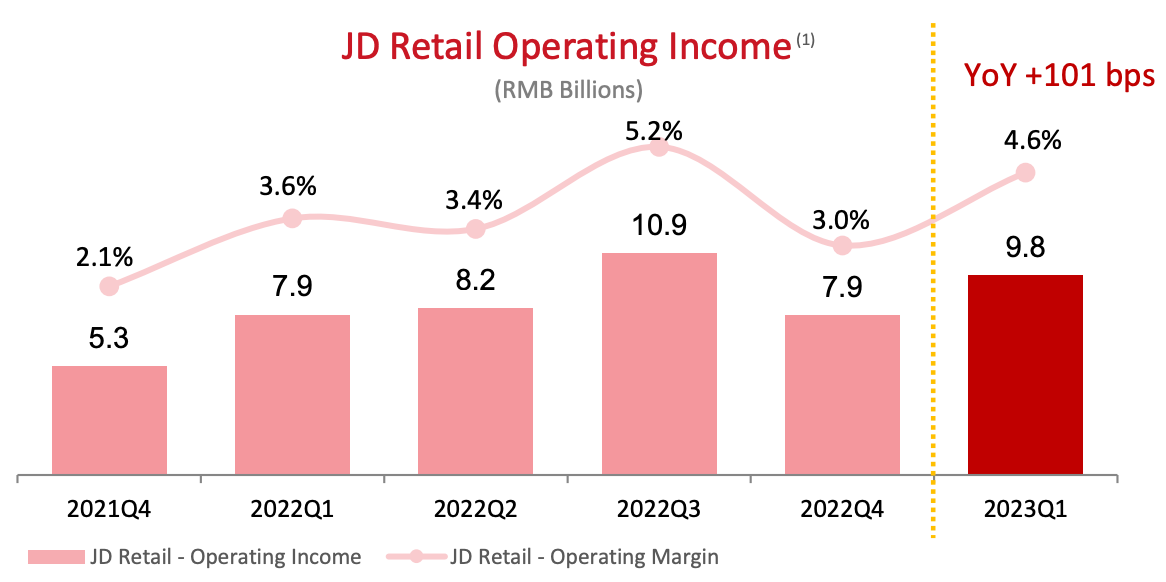

Furthermore, if there’s one positive thing about the government tech crackdown is that it forced tech companies to focus on efficiency within their cost structures. This was clearly visible in the margin increase during Q1 23, driven by operational efficiencies in fulfillment, marketing and R&D expenses. JD has also scaled back on unprofitable new business ventures, putting added emphasis in optimizing the core business.

There should be some offsets to margin expansion, such as the company making further inroads in the lower-margin low income segment, where value-for-money and pricing is a decisive factor. Also, JD is still in investing-for-growth mode, which of course will keep margins and returns on capital relatively low for some time. They have a clear line of sight to the opportunities ahead and are acting accordingly👇🏽

Strong Cash Flow Generation

Because 1P online retail remains the company’s most significant business, margins are quite low on an absolute basis. However, JD’s efficiency and scale allow it to generate a substantial amount of cash, reducing the levels of capital that are tied up in the business. This is why operating cash flows tend to be much larger than operating income👇🏽

JD enjoys significant power in its supplier relationships. Average days payables outstanding were 52.5 days during 2022, for example. They also leverage technology, data and scale to efficiently manage inventory, and customers pay fairly quickly. Average days receivables outstanding and inventory outstanding were 4.5 days and 33.2 days respectively. This means that the company’s cash conversion cycle is (and has consistently been) negative, resulting in strong cash generation.

Compared with a group of strong comparable companies, JD’s cash conversion cycle (“CCC”) is not too shabby👇🏽

Scale Economies Shared

One of JD’s core objectives is providing customers with exceptional value, which often means lower prices combined with top notch customer service. They’re able to do this successfully thanks to the power conferred to them by their scale. JD sources its products from ~45,000 suppliers, leveraging its almost 600 million annual active user base and extensive logistics network to offer the best value possible back to the user in the form of lower prices. Below is a quote from Sandy Xu describing this concept concisely:

This is the famous Scale Economies Shared model pioneered by companies like Costco and Amazon.

This competitive advantage is extremely tough to replicate, particularly thanks to JD’s development of JD Logistics. Going from bits to atoms is incredibly complex, and it requires very different skills as a company. It’s not for nothing that Shopify decided to abandon its effort to build its own logistics operation.

Imitating JD Logistics would be a monumental task that would cost billions of dollars. For JD, it allows unparalleled delivery and customer service capabilities, powered by automation, using billions of data points for 3rd party services.

Valuation

JD trades at a Market Capitalization of ~$55 billion as of May 12th, 2023. Adjust this for the company’s $22.3 billion Net Cash position, and we’re left with $32.7 billion.

2022 Free Cash Flow after backing out Stock Based Compensation is ~$4.42 billion.

This means JD’s operations trade at a FCF multiple of less than 10x. This is very much on the low end of what it has historically been valued at by the market. I don’t like relying much on historical multiples to estimate whether a company is being properly valued today. Companies, and economies, change. But given the reasons outlined above, JD’s valuation looks compelling.

Doing a reverse DCF with a 12% discount rate and 12x exit multiple on FCF ex. SBC, the market is pricing JD’s FCF to contract over the next 5 years. JD will naturally continue to invest throughout this horizon and further, but it’s clear the market is not very optimistic for the company moving forward.

Perhaps it’s related to some of the following risks🫣

Risks

Geopolitical —> an invasion of Taiwan and economic sanctions from Western countries could further depress investors’ appetite for investing in China. An invasion of Taiwan would lead to a situation so serious that I don’t think it would matter where you’re invested though.

Macro —> consumer sentiment in China could remain subdued if the economy does not recover as is expected.

Competition —> JD could burn too much cash competing with Pinduoduo for the lower income market.

Dilution and capital allocation —> JD continues to issue shares, growing ~2% per year, so that needs to be factored in. Repurchases have been minimal, and where not done at good prices, except for the ~$150 million or so done during Q1 23. The company is still in investing-for-growth mode, so as long as they keep mindfully reinvesting cash into the business I think capital will have been well directed.

I think that at these prices investors are being more than compensated for these risks. If I had to pick one risk that worries me the most it has to be competition. Races to the bottom are never pretty, but it seems clear that JD’s management is focused on building a sustainable operation.

I also own Alibaba, but I feel that JD tends to be overlooked when it comes to the Chinese tech space. I would not be surprised if they re-rate in tandem. Overall, JD is a quality company, although easy to miss given the 1P retail model.

If you’re interested in learning more about JD and JD Logistics, Investor Insights Asia has a solid 2-part write-up for each. Links below:

Thank you for reading! Please do your own research whenever you’re considering an investment decision! Feel free to share this post by clicking the button below!