Investment Clones

Investment Clones

The dangers of outsourcing conviction

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice. Also the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

Cloning

I have previously shared some useful websites that let you track the investment portfolios of famous and successful investors:

Thanks to disclosure requirements and the internet, the practice of cloning has gained popularity. Many retail investors today choose to imitate the moves of their favorite investors and copy their portfolios.

These is dangerous, for a few reasons…

Pitfalls

There are a few pitfalls that are not so obvious if you’re not an investments/finance nerd like yours truly.

I’m not a virgin, I swear.

Anyway, one quick point to understand:

Investment managers that manage $100 million or more must file a 13F form with the SEC, detailing the holdings in their investment portfolio and any changes made during the latest quarter.

Of course, most admired/revered (and still active) investors manage more than $100 million, so the mandatory 13F filing is a chance to take a look at their portfolios and any new positions or sales. But…

Pitfall #1: Portfolio disclosure timing can be misleading.

Investment managers must file the 13F form for a quarter within 45 days after the end of the quarter. For example, for the quarter that ends on March 31st, investors have until mid-May to file the form. And most investors file it as late as they possibly can. That’s not an insignificant lag, and it only provides a glimpse into the past.

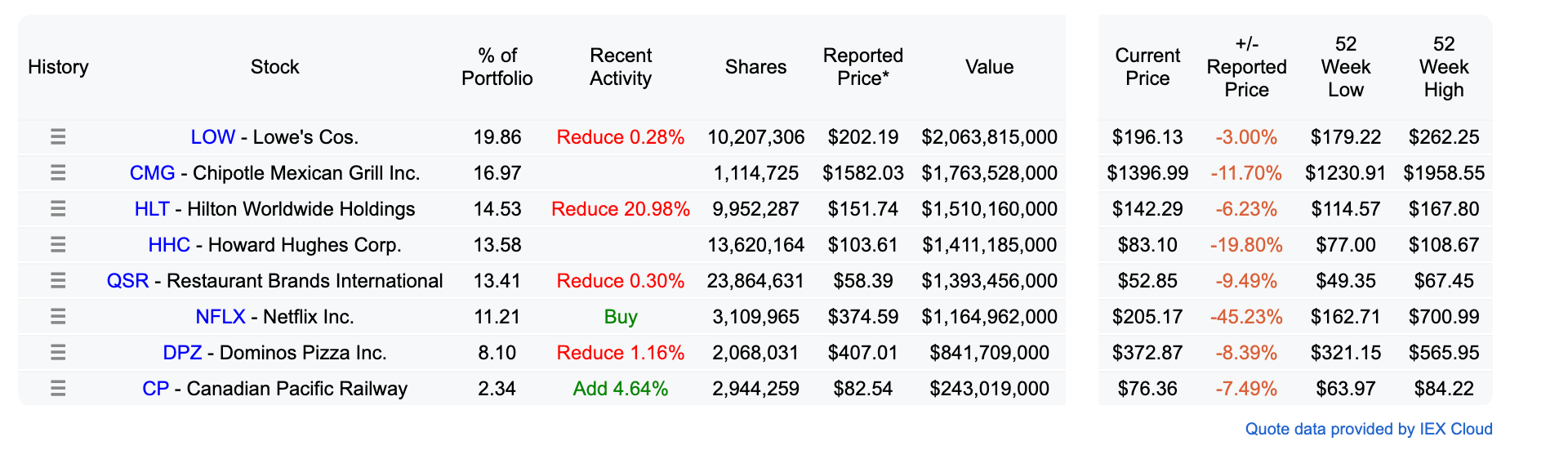

Case and point, if you look in Dataroma, Pershing Square’s portfolio looks like this:

But we know this is not accurate because Bill Ackman (Pershing Square’s manager) publicly announced his sale of Netflix in late April:

Since he sold well into Q2 this move doesn’t show in the latest 13F, because the 13F for Q2 must be filed by mid-July (45 days after the end of Q2 on June 30th).

Most large investors do not publicly announce their trades like Bill sometimes does, so it’s unlikely that their portfolio looks exactly the same as on the day reflected by the filing.

Pitfall #2: 13F filings only require managers to disclose stock positions listed in the US.

Not a minor detail. Investors with global portfolios are only required to disclose their US stock positions, so any position they might hold on a non-US stock will not be reflected. Now, some sources such as TIKR, do provide information on non-US holdings, but they piece it together from other reports or publicly-available data.

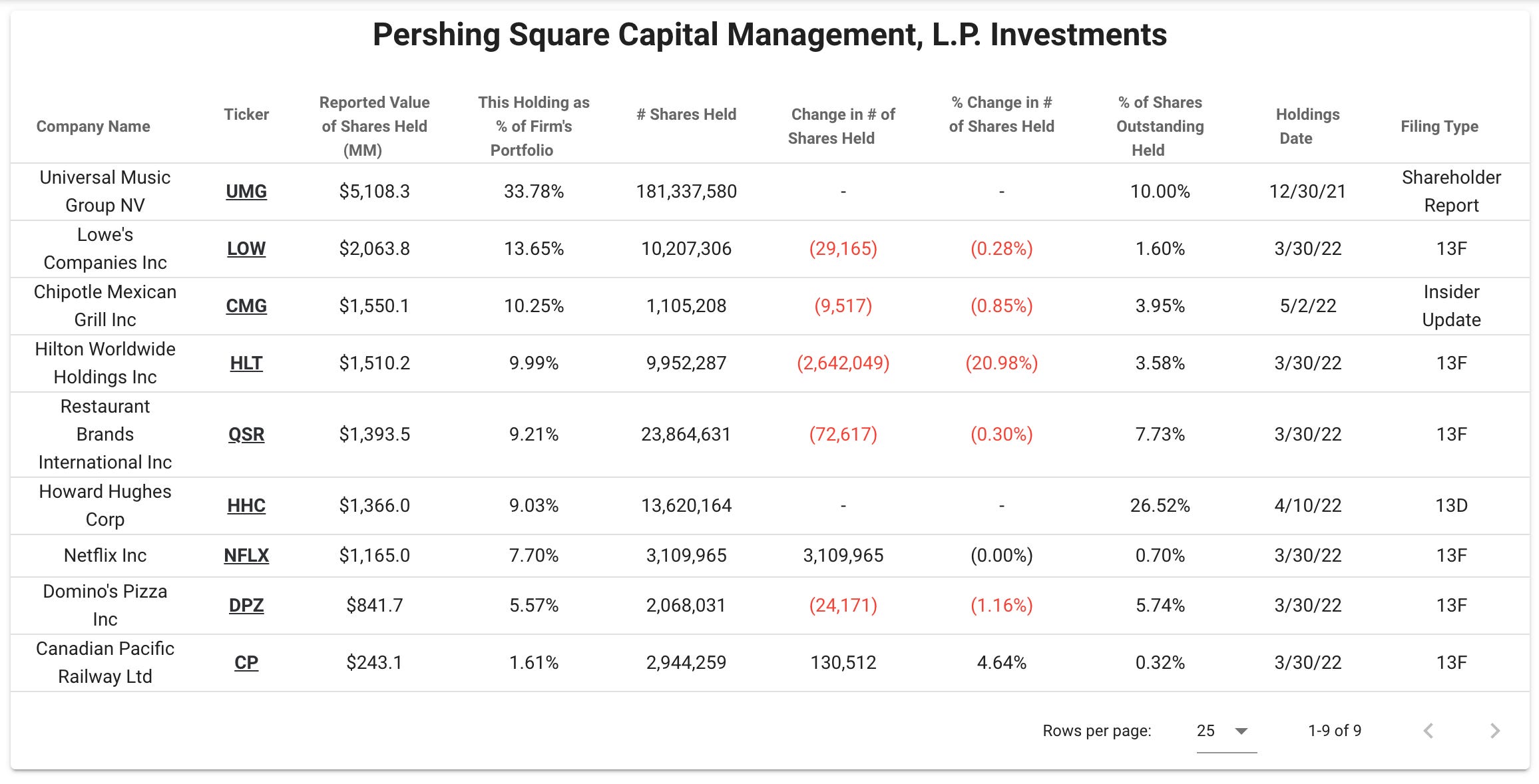

Let’s look at Pershing Square’s portfolio on TIKR:

Universal Music Group is actually Pershing Square’s largest holding, but they’re not required to disclose it in the 13F form because Universal’s shares are listed in Amsterdam, not in the US.

Furthermore, investment managers are not required to disclose most derivatives positions (futures, swaps, warrants, etc.) or short positions (betting against a stock), so the actual exposure might meaningfully differ from the portrait painted by the 13F. Imagine an investor that holds $100 million of US stocks, but is also short the S&P 500 via futures with an exposure of $150 million. His portfolio would be net short (he would gain if the market fell), but you wouldn’t know it from looking just at his stocks.

Pitfall #3: Lack of knowledge about an investor’s strategy (or their particular investment structure) can lead to misunderstandings.

As we mentioned, 13F forms provide a static picture of a single point in time: the portfolio on the last day of a quarter.

But what if an investor has a very active strategy and they buy and sell positions on a daily or weekly basis? Well then, the portfolio can look extremely different from one day to the next, so the 13F form will almost always be a bad portrait of that investor’s portfolio in real time.

So…what about those investors that are renowned for investing for the long-term and are not as active? Well, it’s better. But you can still encounter some issues.

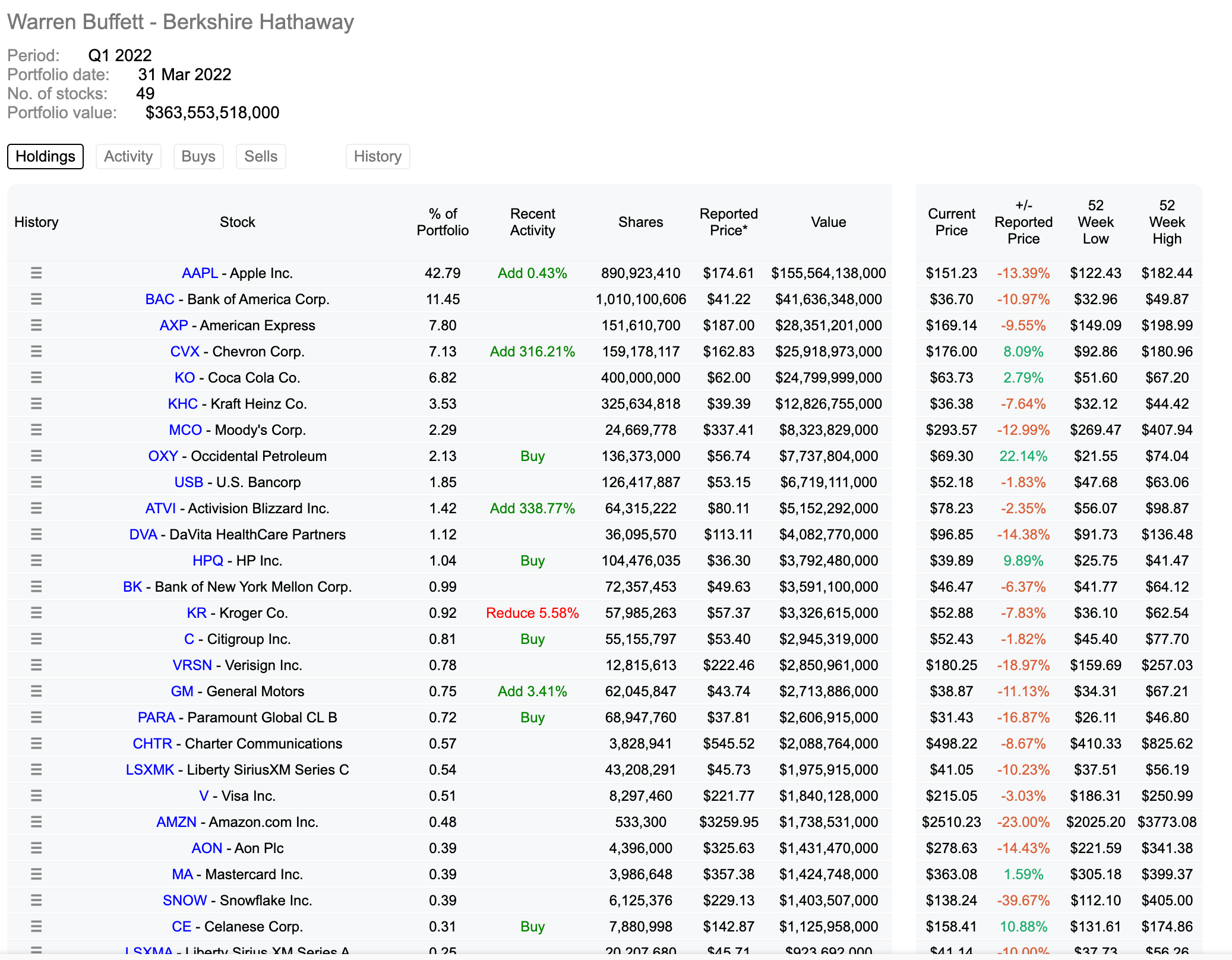

Let’s use Berkshire Hathaway and Warren Buffett as an example. Here’s Berkshire’s portfolio as of March 31st, 2022:

Berkshire’s portfolio tends to be fairly stable, with not much activity quarter to quarter. But…

If you know your Berkshire, you know that Buffett has two lieutenants: Todd Combs and Ted Weschler. Todd and Ted have the authority to allocate a certain amount of Berkshire’s overall cash, well into the billions of dollars. Importantly, they both have different investment styles from Buffett, but in the 13F all of their activity is mixed up into one big portfolio. So if you want to imitate Buffett, how do you distinguish which purchases are his and which ones are his lieutenants’? For some holdings it might be easy. I’d be willing to bet Buffett has been behind the Chevron and Occidental Petroleum purchases since he has invested heavily in energy before. But what about Citigroup? General Motors? Paramount? I have an idea, but it’s definitely not a certainty…

Decision-making

Outsourcing your research and conviction by cloning can lead to sub-optimal decisions. Let’s look at an example to see how this can happen.

Let’s say you really admire Charlie Munger (the guy in the picture below).

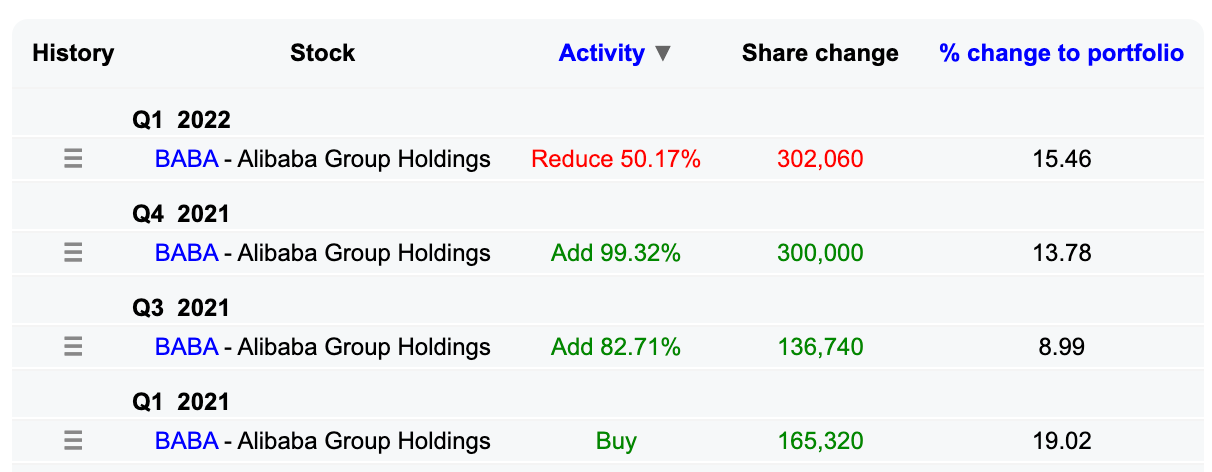

You might have heard about Charlie Munger’s investment in Alibaba, the Chinese big-tech company. Here’s a snapshot of Daily Journal’s (the company controlled by Mr. Munger and his family) portfolio as of March 31st, 2022:

Munger first invested into Alibaba back in Q1 2021 after the company took a proverbial beating due to the disappearance of Jack Ma and more stringent government regulation. A swarm of cloners and Munger admirers then piled into the company as well, following their leader. No due diligence required. I mean, if Munger invested then it’s surely a winner right? RIGHT?

I, being the independent soul that I am, began losing money on Alibaba before Munger did.

As time progressed and Alibaba’s price continued to drop, Munger continued to increase his position. That is… until Q1 2022, when he sold more than half of his shares:

If you were investing in Alibaba just because of Munger, what do you do? How could you know what to do? You probably didn’t do any research and have no idea how the company is doing or whether it’s still a good investment. The fact is, you never knew the reason Munger invested in Alibaba specifically. The reason could be because of some unique piece of information or insight that only he has. Was it ever a good investment in the first place?

Munger is many things, but stupid is definitely not one of them. He could have been tax-loss harvesting when he sold half his shares, but truth is, only Munger knows why Munger sold.

Charlie Munger can also make mistakes, like every investor. And you’re now confused and holding an investment that you have no idea what to do about. Cheers.

Conviction in Investing

That brings me to the importance of conviction when you invest. Now, don’t get confused, conviction will lead you nowhere if it’s just arrogance with a mask.

Another point that many people often miss is that even if you directly outsource your investment decisions to someone else, such as a fund manager or a robo advisor, you still need to understand and have conviction in their strategy. Otherwise, why the hell are you investing with them?

This also applies to following other investors/traders on “social trading” platforms, such as eToro.

So, how can you develop conviction in an investment and go from a cloner to an investor?

Be clear about what it is that you’re doing - are you trading or are you investing? Your strategy and day-to-day will be vastly different depending on what you do. If you invest based on the recommendations of a financial advisor, or if you prefer to outsource your investments using a robo advisor, then you must make sure that you understand and trust their advice/strategy.

Stay within your circle of competence - focus on the industries/geographies/asset classes you have knowledge about. If you don’t know anything about business in China, then don’t invest in China, for example.

Do the work - put your sleeves up and actually research the business, its strategy, competitive advantages, management, capital allocation, etc, etc, etc. This is a continuous work in progress, and it can take you a long time to feel comfortable making an investment. At the end of the day every investment comes with risk, so you have to feel somewhat comfortable with some degree of uncertainty. That’s life.

Thanks for reading! Hope you enjoyed!