Intro

Even though he published it in August of 2023, I only recently found the time to read Aswath Damodaran’s insightful piece on the value of sport franchises as trophy assets:

As an avid football (the one in which you actually kick a ball with your foot) and Formula 1 fan, it has been a little disheartening to experience the encroachment of money into the sports I love. The cynic in me knows that it has always been about money, just not in the magnitude we see today. I have a theory that American sports fans don’t suffer as much from this trend, mainly because over there it has always been more about entertainment and business than about the sports themselves. You do not see ultras in the NFL, NBA, MLB or NHL. While I am on this topic, if you want to see the passion and cultural importance of football illustrated beautifully, I highly recommend COPA 90’s Derby Days videos on YouTube:

Anyway, before I get emotional, today I want to talk about Formula 1 not football. I was surprised when I did not see Formula 1 mentioned in A. Damodaran’s post, especially considering the explosion in the popularity of the sport in the past 5-6 years. Liberty Media acquired the Formula One Group back in 2017 for over $4 billion leading to the sport going through some meaningful changes. Some fans would argue not precisely for the better. While the evolution of the Group itself is fascinating, I also wanted to look at the individual teams and figure out whether it might make sense to purchase one. A man can dream.

As a disclaimer: I swear that I started watching Formula 1 before Drive to Survive. Hand to my heart.

The Formula One Group

F1 has always been a sport in which money plays a relatively large part, both for the teams and the drivers. It’s not cheap to develop the fastest cars in the world, and it’s certainly not cheap to progress through the various categories in motor racing to get to drive one of those cars. The commercial and governance arrangements that make it possible for the sport to exist in its current form are fascinating. The FIA (International Automobile Federation), Formula One Group, and individual Teams are closely related, sharing an interest in the success of the sport, but are ultimately distinct entities.

The Formula One Group, the entity purchased by Liberty Media for over $4 billion in 2017, is the exclusive holder of all commercial rights to the F1 World Championship. It generated ~$3.2 billion of total revenues during FY 2023, up from ~$1.7 billion in FY 2017. While the FIA technically owns the World Championship and is responsible for regulating the sporting, technical, and safety aspects of the World Championship, as well as for every individual circuit, it is the Formula One Group that receives revenues from:

Race Promotion (~29% of total revenues) - race promoters pay for the rights to host, stage and promote each Grand Prix under multi-year contracts. Race promoters then attempt to recover their investment via ticket, product, and hospitality sales. Curiously enough, the Las Vegas Grand Prix is the only event in the Championship organized by the Formula One Group itself.

Media Rights (~32% of total revenues) - this is revenue from television agreements to broadcast F1 events, as well as direct-to-consumer F1 subscriptions (F1 TV).

Sponsorship (~18% of total revenues) - this is revenue from trackside advertising, race title sponsorship, and Global Partner/Official Supplier sponsor packages, generally on a multi-year basis.

Other Revenue (~20% of total revenues) - this includes revenues from various sources, such as facilitating logistics for events outside of Europe (this video is fantastic on the topic), ticket sales to the Paddock Club at most races, support races, and other operations, as well as ticket sales for the Las Vegas GP.

The Formula One Group has a 100-year agreement with the FIA that ensures they remain the exclusive holder to these commercial rights. The agreement expires in 2110. Whoever negotiated that needs a raise. The Formula One Group in turn pays annual regulatory fees to the FIA.

The Teams (Red Bull Racing, Mercedes, McLaren, Ferrari, etc.) are not owned, directly or indirectly, by the Formula One Group. This means they are individually responsible to finance their commitments to be able to participate in the Championship. The Drivers are also directly contracted by the teams, even though they are obviously a main source of attraction for the Formula One Group.

The relationship between the Group and the Teams (as well as regulatory/governance aspects related to the FIA) is governed by the Concorde Agreement, with the latest version signed in 2021. Since it’s in the Formula One Group’s interest to maintain a stable lineup of teams, as well as encouraging some form of competitive balance, this agreement established a Prize Fund to make payments to the Teams based on their performance in the World Championship (based on the Constructors’ Championship, to be more specific). Ferrari, because they’re keen negotiators, and because they can’t win a championship to save their lives, also receives a “heritage” share of the Prize Fund.

As you can see above, the Prize Fund (labelled as “Team payments”) is the single largest cost component for the Formula One Group, amounting to ~$1.2 billion for FY 2023. The final number is calculated based on a percentage of Adjusted EBIT, ensuring that the payments track the commercial success of the sport, to which both the Group and the Teams contribute.

Something that immediately surprised me is how low the Gross Margins are for the Group, at only ~30% for FY 2023. However, it’s clear that if Liberty Media is indeed interested in increasing the long-term value of the business then they should ensure they take care of the financial health of the Teams. Operating margins were a respectable 12% though, and with Team payments capped at a % of Adj. EBIT and decent amounts of operating leverage from the stable SG&A base, there might even be some room for margin expansion, provided the popularity of the sport continues to grow…

The second thing that popped to my mind was the substantial increase in “Other costs of Formula 1 revenue”, which are mostly “costs related to promoting, organizing and delivering the Las Vegas Grand Prix, hospitality costs, and costs incurred in the provision, and sale of freight, travel and logistical services". The FIA regulatory fees and some other costs such as television production are also included there. There were the same number of races in 2023 and 2022, and logistics costs actually fell during 2023, so it’s clear that the bulk of the spike was related to the costs of the Las Vegas Grand Prix.

There was, of course, a revenue increase from tickets and the like, but it illustrates the strong push the Group is making into cracking the US market for F1. Surely it would have been more profitable to find a pre-existing circuit and a promoter in another city in the US, but it wouldn’t have generated the buzz of Las Vegas.

At this point, with 23 races in the calendar, the Group doesn’t have much room to add more races, both because of logistics and the fact that at least 70% of the Teams have to provide consent if there are to be more than 24 Events in a season. Continued increases in revenues will then be dependent on eyeballs, which in turn will help with higher promotion contract fees, a bump in media rights revenue, and demand from sponsors.

F1 Teams

Scuderia Ferrari

Ferrari is, in every regard, a special participant in the F1 Championship. It’s the only team to have competed in every edition since 1950, and it has both the most Constructors’ Championships (16) and Drivers’ Championships (15). The company was founded by Enzo Ferrari to race cars. Its origins are firmly rooted in motor racing.

However, what started as old Enzo’s passion, is not the main focus of the company. As they themselves write in their annual report:

“Formula 1 racing allows us to promote and market our brand and technology to a global audience without resorting to traditional advertising activities, therefore preserving the aura of exclusivity around our brand and limiting the marketing costs that we, as a company operating in the luxury industry, would otherwise incur.” - Ferrari, Form 20F, 2024. SEC filings.

Said differently, because regular advertising is beneath Ferrari, they use their F1 team as their marketing. I’m not going to write extensively about what everyone already knows: Ferrari is one hell of a company. It generated EUR 5.9 billion in revenues in 2023 while selling less than 14,000 cars. The company boasts almost 30% operating margins and similar returns on invested capital. And it possesses one of the strongest, most recognizable brands on the planet, if not the strongest.

Unfortunately, even though Ferrari is a publicly-traded company, there’s not that much detail on their F1 division financials. F1 revenues are included within “Sponsorship, commercial, and brand” revenues, alongside other racing divisions and licensing of the brand for merchandise. This represents only ~10% of total net revenues. The annual growth rate of this line has been quite anaemic since 2015, growing from ~EUR 441 million to ~EUR 572 million today, or ~3% per year. Revenues have been growing at low double digit levels for the past 2 years, but it’s tricky to find out how much is attributable to the F1 team.

It’s also impossible to calculate operating margins, as F1 racing team costs are lumped within Selling and R&D expenses for the whole firm in their financial statements. That said, if the company considers their F1 team as marketing, then their calculations on ROI would go far beyond the operating income of the team in isolation. It’s clear that they consider both commercial and competitive factors in deciding things such as who will drive for the Scuderia. As does every team, to be fair. Ferrari doesn’t have to worry about generating profits for the division to make an investment case though.

Mercedes AMG-Petronas

While Mercedes competed for 2 years in the 50s as Daimler-Benz AG, actually winning the Championship on both years, they were then absent from F1 until 2010 when Daimler bought a minority stake in Brawn GP. After a few years of adjustment the team went on to win a record 8 Constructors’ Championships in a row from 2014 to 2021.

They have struggled since. I’m using the word “struggle” lightly. They’ve finished 2nd the past couple of years. Unlike Ferrari, the Mercedes-Benz Group do not own 100% of the Mercedes F1 team. Since 2020, ownership has been split between 3 equal partners:

Ineos Industries Holdings, a large chemicals company owned by billionaire Jim Ratcliffe, owns 1/3.

Mercedes-Benz Group, via Mercedes-Benz Holdings UK, owns 1/3.

Toto Wolff, team principal and CEO, owns 1/3. Wolff originally came on board in January 2013, purchasing a 30% stake in the team.

Incorporated as a limited company in the UK, Mercedes-Benz Grand Prix Ltd. must file public financial statements with Companies House, which reveals interesting details about the business of a top F1 team.

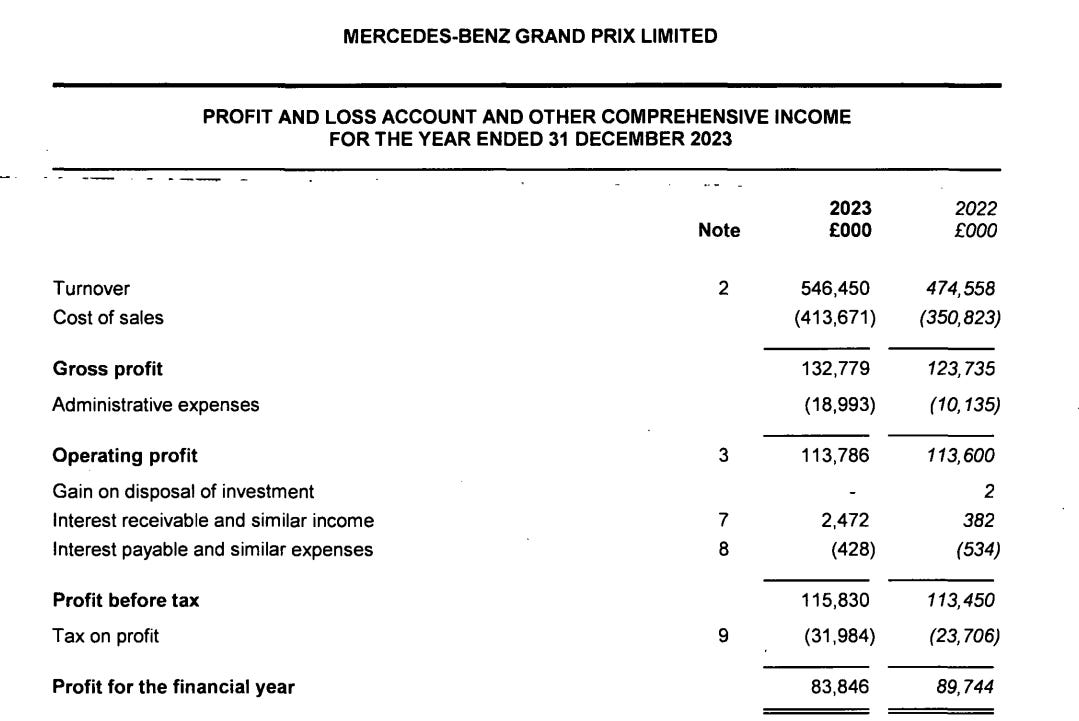

The Mercedes F1 team generates almost GBP 550 million in revenues, the vast majority of which relates to sponsorships and prize money. Sadly they don’t break it down in detail aside from separating the portion attributable to services (~GBP 495 million) and goods (the rest). Back in 2013, total revenues were closer to GBP 125 million. This means the top line has grown at ~16% per year since 2013, when Toto Wolff first took over. This also coincides with a change in F1 car regulations, which in turn resulted in a dominant decade for Mercedes.

Similarly to the Formula One Group, gross margins are low at ~24%. The company includes both the bulk of employee expenses and R&D costs within Cost of sales, which is sensible considering those are essential to compete and generate revenue. Employee expenses of GBP 127 million include the drivers’ salaries, which are by far the largest ones in the company. However, here’s where things get more interesting. Gross profits were negative back in 2011, 2012, and 2013. This goes to show the investment that was necessary to get the team to a position where they could achieve consistently good results on the track.

That said, the administrative expense load is so small that gross profits almost fully flow through down to operating profits, so operating margins come in at over 20%. What’s better, it seems a decent chunk of these profits are being converted to cash. They experienced some adverse working capital movements in 2023, but if I average operating cash flows for 2023 and 2022 I get to ~GBP 110 million in OCF, or ~95% cash conversion. Average capex for the two years was ~GBP 35 million, leaving ~GBP 75 million in free cash flow for the 3 shareholders.

And this is where I get to perhaps the thing that surprised me the most about Mercedes as a business: they run the company without leverage. I’m not sure whether this is deliberate timing considering the changes the team is going through, and the looming new regulations for 2026, but it’s a sign of conservatism rarely seen in business these days.

At a somewhat superficial glance the Mercedes F1 team looks like a lovely cash-generating, debt-free business run by an owner-operator. They also share a couple of interesting data points in the report:

The team’s share of TV coverage is ~14.7% during 2023, a small decline compared to 2022 due to the lower number of podium finishes.

They had 36 million cumulative social media followers, with 465 million engagements during 2023, increases of 15% and 9% respectively compared to the previous year.

These two points get to every F1’s team main issue: uncertainty. Lewis Hamilton, one of the world’s most popular drivers, is leaving Mercedes in 2025. Regulations are changing in 2026. Will the sport continue to gain in popularity? How much will these issues affect Mercedes' position in the standings and in fans’ hearts? How will that translate to eyeballs?

In July 2023, Forbes published a piece estimating the “value” of F1 teams. If you read Damodaran’s piece you’ll know why I put “value” in quotation marks. In that article, Forbes estimated Mercedes’ “value” at ~$3.8 billion, based on an EBITDA estimate of ~$192 million, or a 20x multiple. In reality, FY 2023 EBITDA came in at GBP 92.5 million or ~$120 million. Forbes’ estimate would then be closer to a 30x EBITDA multiple. I know that these “values” tend to be based on comparable transactions, and that there’s now a trophy asset element to these teams, but it does seem a bit rich. For reference, Ferrari stock is trading in the market at ~36x LTM EBITDA, although that includes one of the best luxury businesses in the world. In any case, most people would call that overpriced too.

Red Bull Racing

I honestly wanted to do an analysis of McLaren instead of Red Bull because of the team’s heritage. Unfortunately, Mercedes is the only team that has filed their accounts for 2023. The deadline is September 2024, so I’ll take that as more of a green flag for Mercedes than a red flag for everyone else. McLaren’s 2022 season was pathetic so, spoiler alert, they lost money. As did Aston Martin and Williams.

Alpine Racing made a profit in 2022 and 2021, but I’ve already looked at Ferrari as an example of a wholly-owned F1 racing team (not that I’m equating Renault to Ferrari). That said, Alpine is a case I want to look at in detail once they file their accounts. They finished 5th - 4th - 6th in 2021-2022-2023 respectively, and are currently 8th so far in 2024, so they will be an interesting case study on how performance affects financial results.

Just to round up the rest, Haas is an American team with entities in the US, UK and Italy, V-Carb (or however the fuck it’s called) is an Italian entity, and Sauber is a Swiss entity, so I can’t access their financial results anywhere because they’re private.

Anyway! Since I had to choose from a set of accounts for 2022, I figured Red Bull’s might be the most insightful since they won the World Championship in 2013 and 2022, making for a nice little comparison.

The first thing that immediately caught my eye in Red Bull Technology Ltd.’s 2022 strategic report is the following line:

“ORBR attracted 22.1% share of global television coverage in 2022, more than any other F1 team.”

Mercedes’ share of TV coverage in 2022, a year in which they finished second, was 15%. Red Bull had a dominating season in 2022, which resulted in a 30%(!) delta in share of TV coverage with the 2nd placed team. This has to be an incredibly strong hook to catch valuable sponsors, which goes to show how Mercedes was able to grow their top line so strongly during the past decade.

Moving to the financials, Red Bull generated GBP 385 million in revenues during 2022, a 13% increase from 2021, a year in which Max Verstappen won the Drivers’ Championship but Red Bull finished second behind Mercedes in the Constructors’. They did this while earning a ~22% gross margin and a meager ~3% operating profit margin. EBITDA margins were close to double operating margins.

Compared to Mercedes’, Red Bull’s administrative expenses are a much larger proportion of revenues. Overall, for 2022, Red Bull spent ~GBP 370 million in Cost of sales and Admin expenses, compared with ~GBP 360 million spent by Mercedes in the same items but on a much larger revenue base of GBP 475 million.

Comparing 2022 with 2013, Red Bull’s revenues have grown at just over a 4.5% CAGR. Operating profits have grown at a 5% CAGR, from ~GBP 9.8 million to ~GBP 15.3 million.

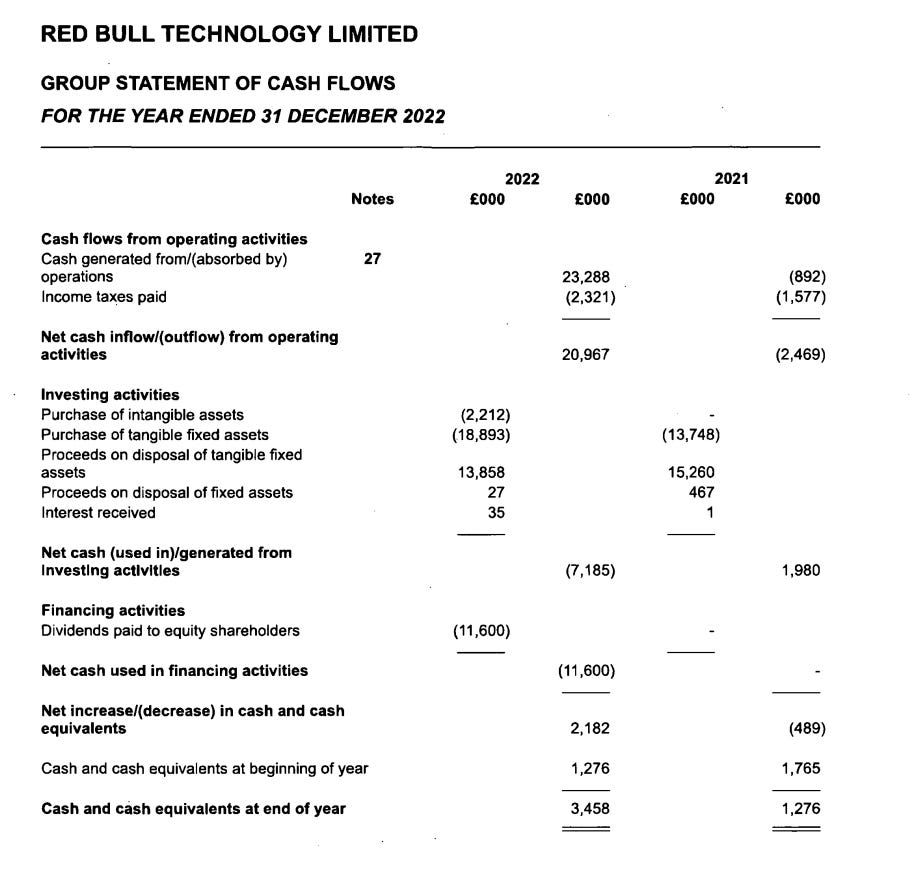

When it comes to cash flows, the company produced ~GBP 18 million in cumulative operating cash flows throughout 2022-21. Capital investments of ~GBP 33 million during the same period fully offset these inflows. Similarly to Mercedes, Red Bull had no debt on its balance sheet although it did owe ~GBP 30.2 million to “group undertakings”, which refers to Red Bull GmbH (Red Bull’s Austrian parent company). It looks like Red Bull F1 is probably leveraging the parent’s balance sheet to maintain efficient operations.

It seems like there is a long time lag between success in the track and strong top line growth, especially in regards to sponsorship revenue. Red Bull closed Oracle as its main sponsor in early 2022, so it could be possible there wasn’t such a strong ramp up until 2023.

Red Bull appears to be in more of an investment mode compared to Mercedes, although it will be fascinating to look at 2023’s numbers once they’re filed. Perhaps there was a normalization once Red Bull cemented themselves as the top dog of the current era. In the Forbes article I linked above, Red Bull F1’s 2023 EBITDA is estimated to be $85 million. This would be a large jump from 2022’s level of close to ~$40 million. Assuming a more conservative jump to $60 million in EBITDA for 2023 the Forbes “valuation” of $2.6 billion would represent a multiple close to 40x EBITDA. Even using their own estimate of $85 million, we’re talking about 30x EBITDA. With new regulations looming in 2026, I wouldn’t be so sure to pay that…

The team is not so different from Ferrari, in the sense that it serves as strong marketing for the parent company’s main product. I guess the fact that it turns a modest profit is just the icing on the cake.