Dharma of Capital X

Housekeeping

Like always, it goes without saying that what I write in these posts is not financial advice, and the opinions here are solely my own.

Is Europe Good Value?

Lovely days in the market, courtesy of the Omicron variant. *Insert overused Black Friday Sale joke*. Won’t really spend time talking about this sell-off. Personally, I think new variants at this point should not be of much concern to governments or the market, but panic sells I guess. Instead, I prefer to focus on potential long-term opportunities.

I have been wondering whether European stocks are actually good value at the moment. Morgan Stanley, JP Morgan, and Goldman Sachs seem to think so.

“We retain a positive outlook on European stocks for 2022. (Europe) represents good value versus the U.S. and excellent value versus other assets.” - Goldman Sachs

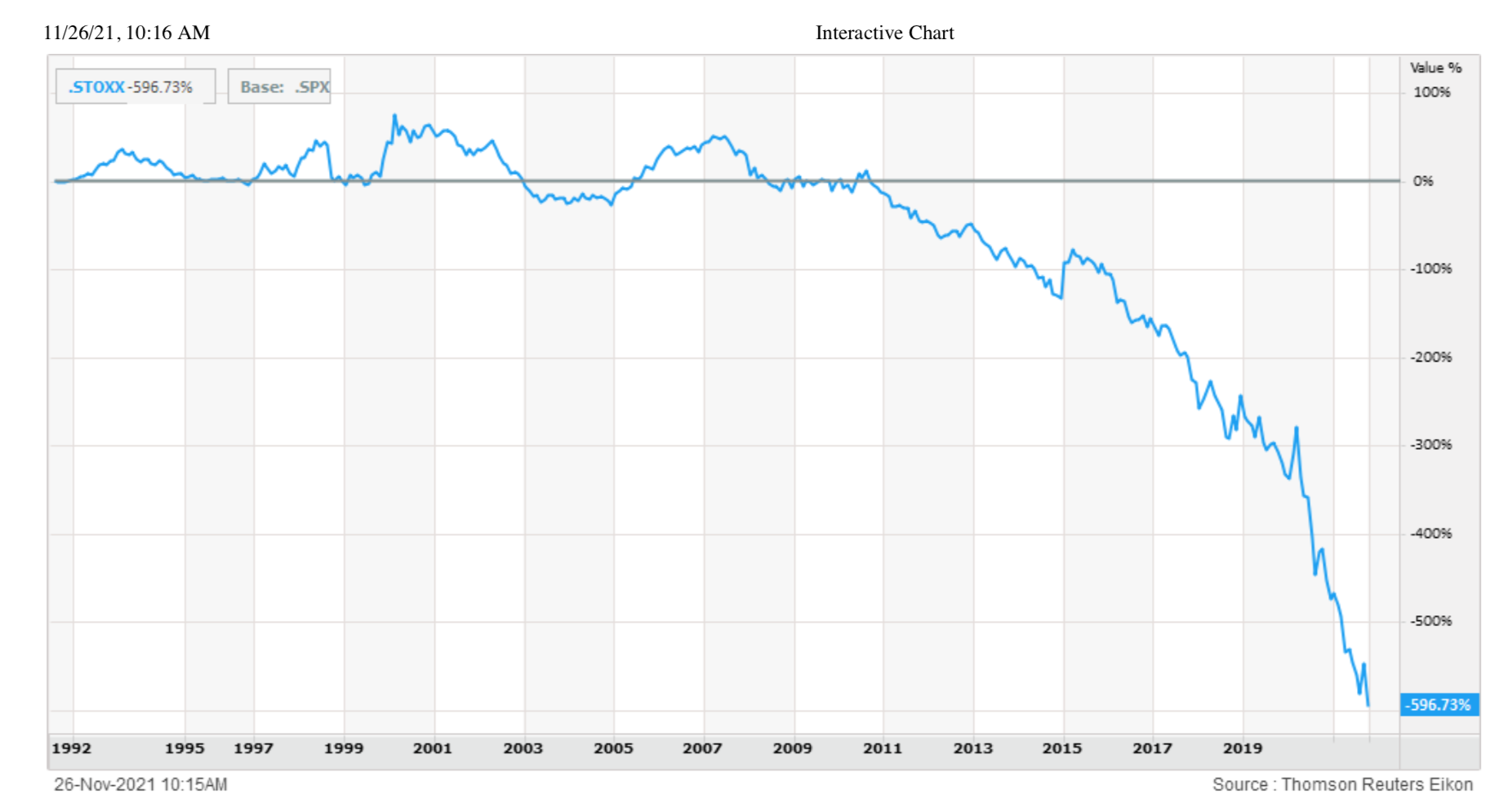

Performance-wise, Europe has been a massive disappointment for some time now, at least relative to the US:

To be fair to Europe, the whole world has underperformed the US during the past decade:

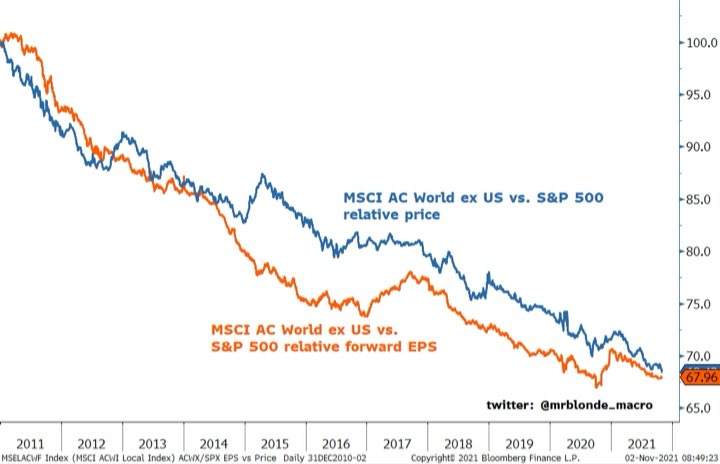

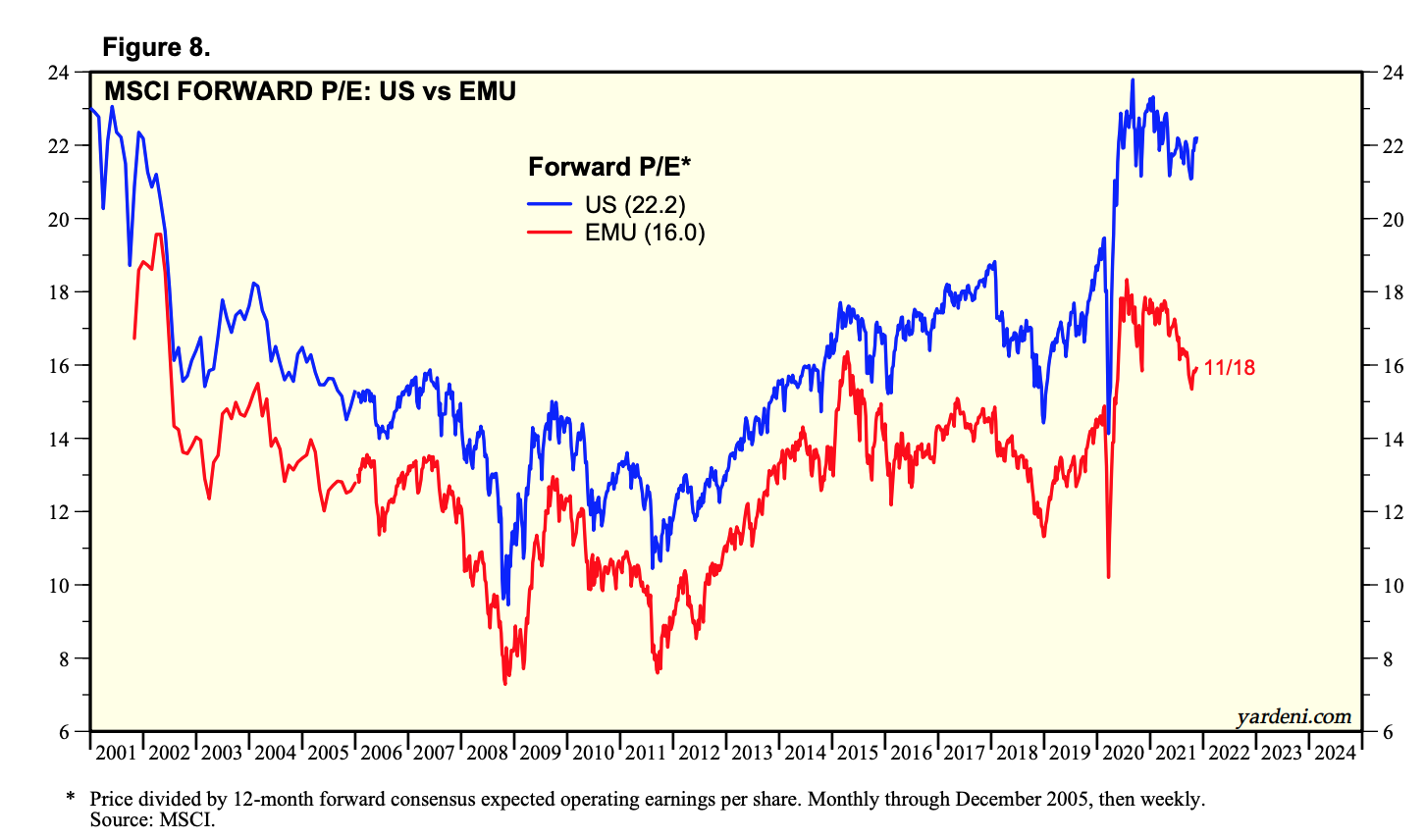

Valuations do look more attractive in Europe if we compare the broad indices on a forward P/E basis:

The spread is even more dramatic vs the UK:

It’s good to remember that cheap does not equal attractive. If anything, during the past decade “cheap” has been very good at getting cheaper.

But… 2022E earnings growth rate (3rd column below) does seem to show promise for the EMU (European Monetary Union), showing 8% expected earnings growth vs 7.3% in the US. The UK still looks extremely disappointing though.

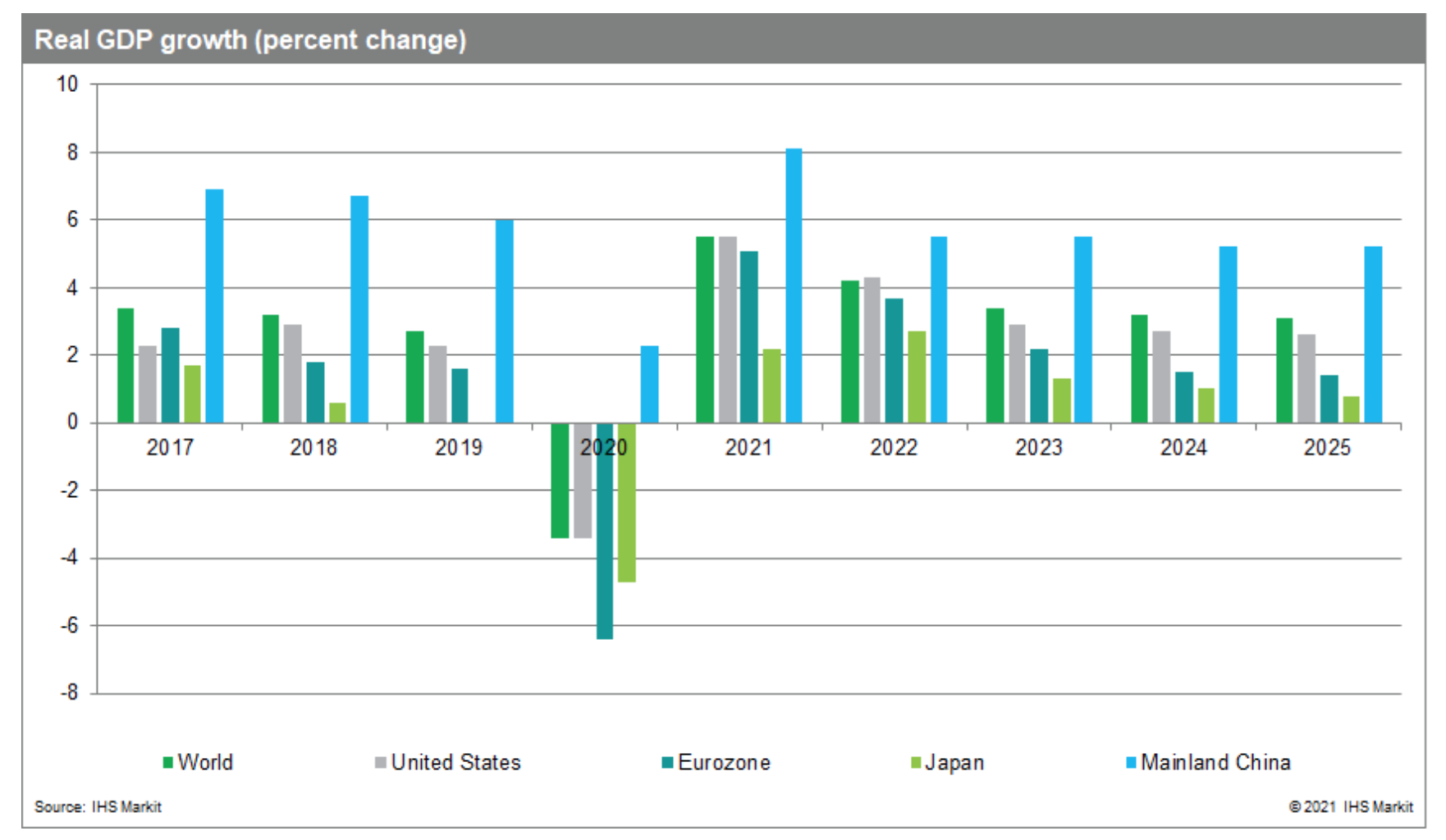

On the flip side, real GDP growth is expected to be higher in the US than in the Eurozone for the next 4 years. This is true even though the Eurozone experienced a rougher contraction during 2020:

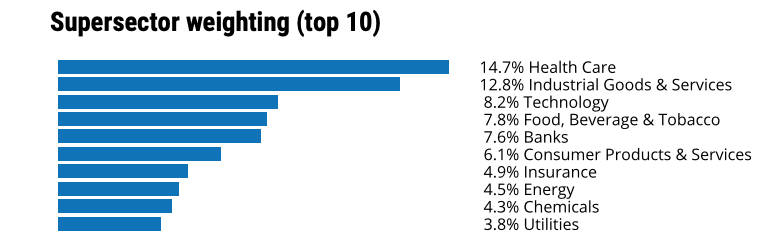

Furthermore, it’s no surprise to see cheaper valuations in Europe when considering the composition of its indices. While technology represents a hefty percentage of the S&P 500, it is a much smaller portion of the STOXX 600. Tech stocks tend to receive loftier valuations thanks to higher growth expectations.

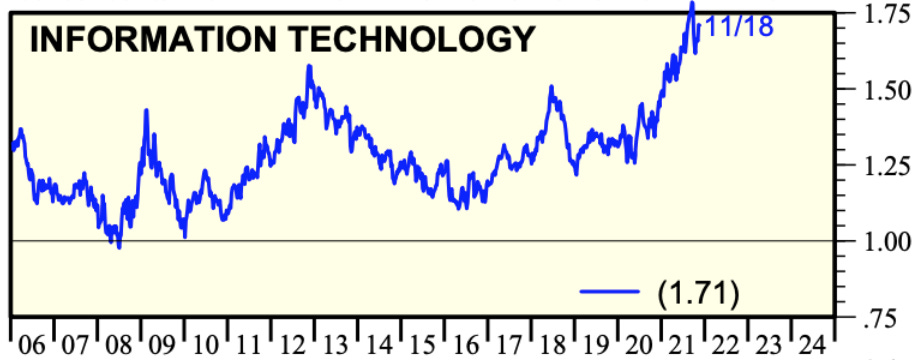

Funnily enough, when we look at the valuations of the Technology sectors in each region they’re actually higher in Europe than in the US. Below you can see the valuations relative to the MSCI All Country World index for both the EMU and US Technology sectors.

One big caveat here. In the US, Amazon and Tesla are part of the Consumer Discretionary sector, while Meta and Alphabet are part of the Communication Services sector, so some companies that would most likely push valuations higher in the US are excluded in this comparison. Unsurprisingly, the above comparison for every other sector shows that European sectors are cheaper than their US equivalents.

Also unsurprising, these sectors in Europe are composed of “old economy” companies that engage in more traditional businesses: luxury goods, apparel, auto manufacturing, and traditional telecommunications. It seems to me that a big part of the difference in valuations arises from the fact that the US is simply superior in terms of technological innovation, and this shows in the indices. This doesn’t mean that some of Europe’s “old economy” businesses can’t be undervalued solid long-term plays.

I would own European stocks as part of a diversified long-term indexed portfolio, but I wouldn’t think of overweighting the region. I recognize the real possibility of mean reversion in US stocks, but given the nature of the current financial system I struggle to see a scenario in which European stocks hold up well while the US sells-off or underperforms for a prolonged period of time.

I would take a closer look at Europe for stock-picking. Would not be surprised to find some undervalued gems in that haystack.

One Up on Wall Street

Speaking about stock-picking. I’ve just finished reading Peter Lynch’s One Up on Wall Street. He ran the Fidelity Magellan fund for 13 years, between 1977 and 1990. During this time the fund returned 29% per year and outperformed the S&P 500 by a wide margin.

Lynch specialized in active management by picking individual stocks, and he ran a portfolio of thousands of holdings! One very useful framework he used was to divide stocks into 6 categories, emphasizing the importance of knowing which category a particular stock belonged to because it defines the drivers of the story. The 6 categories are:

Slow Growers - these are companies in declining industries, growing at most at 2-4% per year. According to Lynch, you buy these (if you even consider it at all) for the dividend, and so it’s key to check the sustainability of that dividend.

Stalwarts - “not exactly agile climbers, but faster than slow growers”. Expect around 10-12% annual growth in earnings. The key issue with these is the price you pay. Lynch recommends looking at the P/E ratio, at whether the company is engaging in dubious acquisitions, and at the long-term growth rate.

Fast Growers - Lynch’s favorites. These are “small, aggressive new enterprises that grow 20 to 25% a year”. In a small portfolio, one or two of these can make a career, since they can end up being 10-to-40 baggers. Importantly, a fast-growing company doesn’t necessarily have to be in a fast-growing industry. Lynch focuses on whether the growth is sustainable and whether the company has a good balance sheet. “The trick here is figuring out when they’ll stop growing, and how much to pay for growth”.

Cyclicals - companies with sales and profits that rise and fall in regular if not completely predictable fashion <usually in line with the business cycle>. Autos and airlines are examples of cyclicals. Timing is everything with cyclicals, as well as the ability to detect signs of falling off or picking up in the business. Dangerously, because cyclicals are usually large and well-known companies (think Ford or American Airlines) they can get mistakenly lumped together with stalwarts.

Turnarounds - these are companies on the brink of bankruptcy. Turnarounds often fail to materialize, but when they do they “make up lost ground very quickly”. The most important question here is: can the company survive a raid by its creditors? It’s also important to familiarize oneself with the debt structure of the company, whether their business is coming back, and whether the company is cutting costs. Not an easy feat to correctly gauge a turnaround, but if done effectively it can be very rewarding.

Asset Plays - companies that own one or a few very valuable assets that are worth more than the entire company’s market value. Think companies that own precious metal deposits, real estate, land, rights or extremely valuable brands, for example. Two questions are key here: 1) what’s the value of the assets, and 2) is there any debt to detract from this value? I think asset plays used to be easier for retail investors, since Wall Street overlooked many such opportunities. I personally think these might be much harder today.

Know what you own, or plan to own, and it will be easier to identify the main drivers that will carry your thesis forward!

Thank you for reading! See you in the next edition!