Alimentation Couche-Tard Inc Investment Thesis

CVS Consolidator

Housekeeping

As a quick disclaimer, what I write in these posts is not financial advice. Also, the opinions here are solely my own and they don’t represent the views of any company I might be affiliated with at the time of writing.

I encourage you to do your own research on every potential investment. I’m comfortable with my portfolio, but none of my holdings are investment recommendations. I own Alimentation Couche-Tard shares, bought at an average price of just under CAD 77 per share.

Investment Thesis: Alimentation Couche-Tard

Quick Introduction

Alimentation Couche-Tard is a multinational operator of convenience stores. The company was founded in 1980 in Laval, Quebec, Canada, by Alain Bouchard, Jacques D’Amours, Richard Fortin and Réal Plourde. After acquiring 11 “Couche-Tard” (“night owl” in French) stores in Quebec City, the firm has grown rapidly mainly through various acquisitions. It entered the US market in 2001 and the European market in 2012.

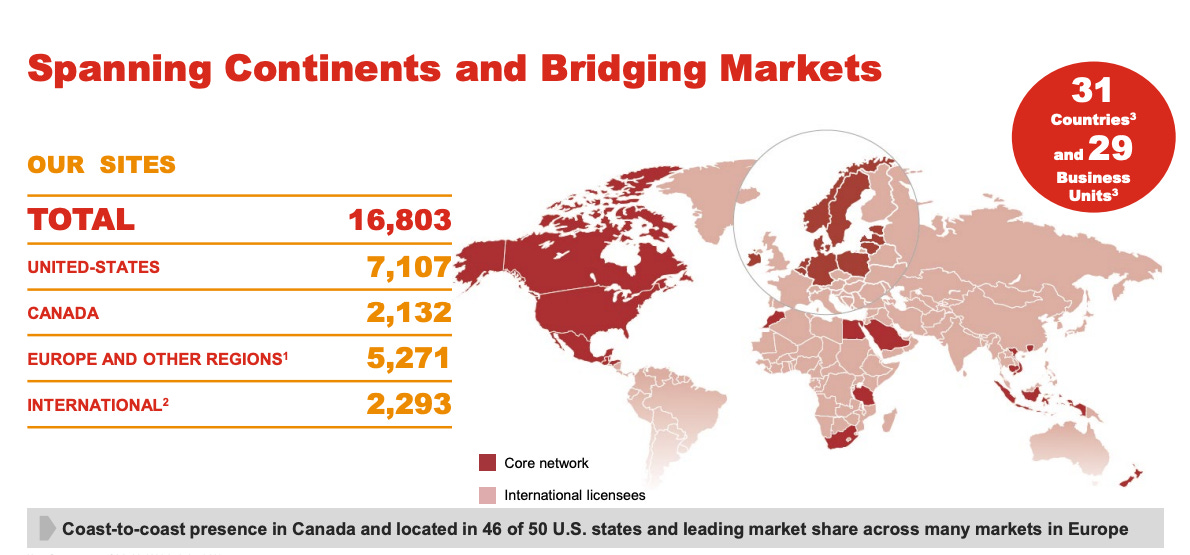

Currently, Alimentation Couche-Tard operates almost 17,000 stores in 31 countries across 29 business units. The majority of their stores, particularly in the US, are under the Circle K brand, which they acquired in 2003. Close to 2,300 stores are licensed internationally, while ~7,400 also sell fuel in a gas station format. Below is a snapshot of their global footprint.

74% of revenues come from the sale of fuel, while 25% comes from the sale of merchandise and services in the stores. However, gross profits are roughly split in half because fuel margins are much lower than merchandise margins.

Investment Case

While margins are on the low-end (average pre-tax margins for the last 3 years are ~5.3%), returns on capital employed are quite decent at ~16%. Returns on tangible capital employed are even higher in the low 20s.

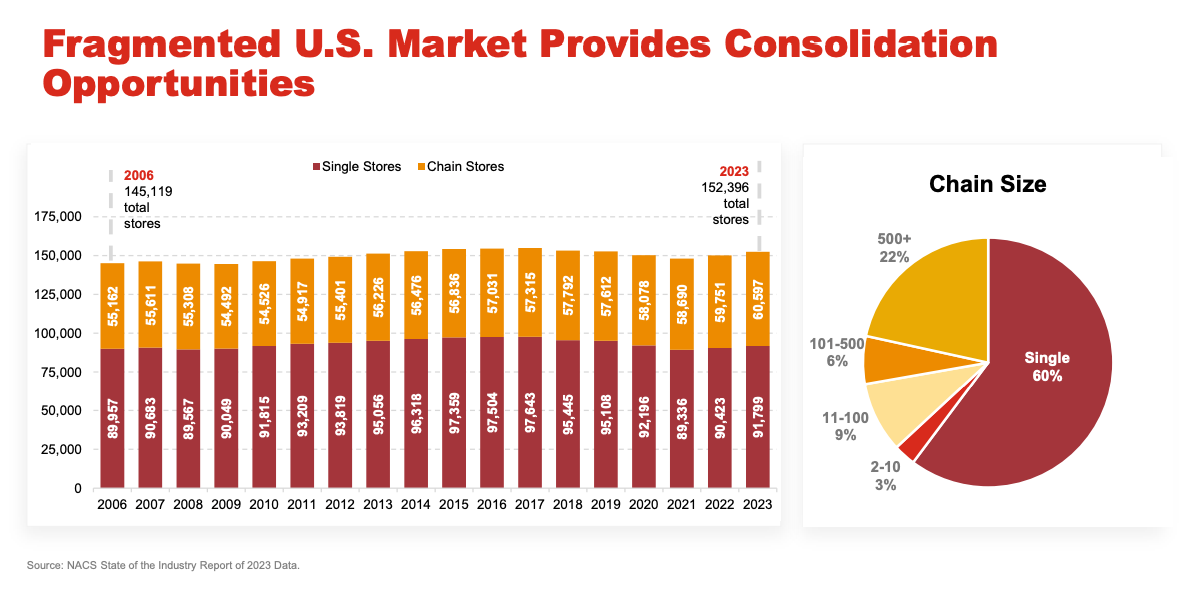

Alimentation Couche-Tard operates in a highly fragmented industry, which is growing, but not at a fast-enough pace to attract new competition.

For example, close to 60% of convenience stores in the US are owned by single-store operators (“mom n’ pop shops”). These single-store operations are much less efficient than those of chains, such as Circle K. While the situation is a bit different in Europe, it is also a fragmented market. Moreover, many of the chain store operators are oil/energy companies that do not consider the stores as core to their operations, so they make for attractive sellers.

Source: ATD Q1 25 Investor Presentation. This means Couche-Tard’s reinvestment runway is fairly long, and they can book some easy wins thanks to their expertise in making store operations efficient and leveraging the scale of their fuel supply chain.

When they don’t reinvest cash at attractive returns, they return it to shareholders via a small dividend and share repurchases. They’ve reduced their share count at an average rate of 3% during the past 5 years.

Alimentation Couche-Tard benefits from being a low-cost operator with efficient operations that generate strong returns from scale. The nature of the products they sell (quick food, beverages, cigarettes, and fuel) make the business fairly resilient to recessions.

The company is conservatively run and financed. Net debt to EBITDA is ~2.2x, and they protect their investment grade rating. They usually increase leverage when they make a relatively large acquisition, but then they subsequently deleverage as they continue generating stable cash flows.

Source: ATD Q1 25 Investor Presentation. Importantly, all of the 4 founders remain active in the Board of Directors, and own close to 20% of the shares between them. Alain Bouchard, the Chairman and former CEO, alone owns ~13% of the shares outstanding. Jacques d’Amours is indirectly involved. His foundation is represented on the board by his daughter, Marie Eve.

Operations are fairly decentralized, and they do a great job at promoting talent from their acquired businesses.

The company is currently selling for a ~USD $53 billion market capitalization, ~USD $65 billion enterprise value. Free cash flow at the moment is somewhere between USD $2.5-$3 billion (the fuel component can lead to some short-term volatility).

Assuming free cash flow grows in the high single digits during the next 5-7 years, a multiple of 18x-20x FCF, and a small benefit from repurchases, annualized returns from today’s prices (CAD 77-79) can get to the mid-to-high teens, for a high-quality business with a long reinvestment runway, conservatively financed, and run by aligned and capable managers.

Main Risks

The Seven & i Holdings deal.

This is probably the main short-term uncertainty around Couche-Tard at the moment. It was revealed in Aug 2024 that Couche-Tard had made an unsolicited bid to buy Seven & i Holdings, the Japan-based owner of the 7-Eleven chain of convenience stores. The original offer of $38.5 billion was rejected by Seven & i’s board. Couche-Tard subsequently submitted a higher proposal of $47 billion. However, the latest news is that Seven & i is exploring a $58 billion management buyout, supported by the founding family, other investors and the largest Japanese banks.

The size of the deal has some Couche-Tard investors worried. $47 billion would be, by far, the largest acquisition in the company’s history, and a massive integration effort. It would also mean that not only would Couche-Tard have to significantly increase their debt levels, but also issue some equity to fund the deal. At the $58 billion valuation implied by the potential, unfinished management buyout offer, the additional equity requirement would be even more demanding. I’m unsure whether Couche-Tard’s management would push for an offer that matches or improves on the $58 billion MBO.

I believe that Couche-Tard will walk away at the wrong valuation. In that case, the reinvestment runway is still long with plenty of opportunities in the US, Europe and beyond. In the meantime, the company would continue repurchasing shares at attractive levels.

However, even if Seven & i is able to push Couche-Tard to improve their current bid, and if the deal is able to go through anti-trust regulators in both Japan and the US, Seven & i’s operations would be a strong addition to Couche-Tard’s at the right price.

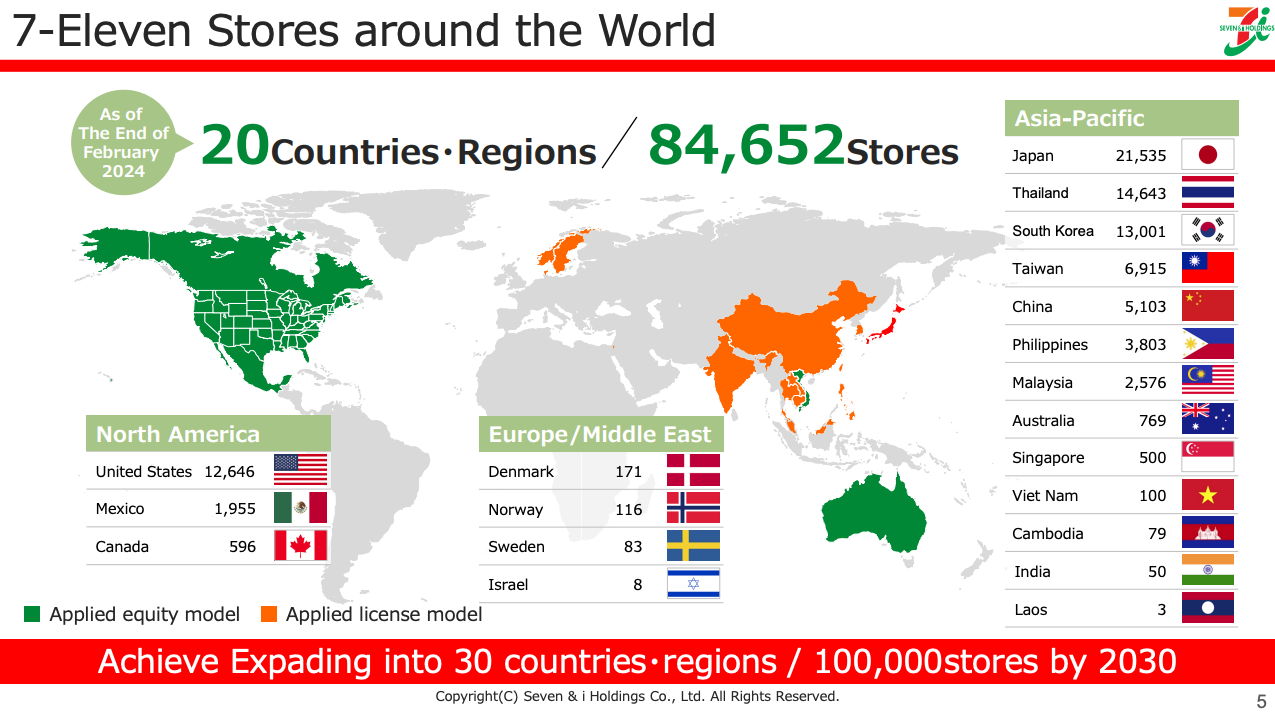

Source: Seven Y i Holdings 2024 Investor Day Presentation. The Japanese convenience store business is Seven & i’s crown jewel and its largest operation in a single country, with leading market share and close to 30% operating margins. The majority of the stores are under franchise agreements, and convenience stores are ubiquitous in Japan. 7-Eleven Japan is renowned for its product quality and strong supply chain.

Source: Seven & i Corporate Outline Presentation. The US business (part of their “Overseas convenience store operations” is the market share leader in convenience stores in the country, with close to 9% market share. Seven & i’s current strategy aims to improve the operations and offering of their US convenience stores, as there’s an enormous gap in the quality between their Japanese and American businesses. Couche-Tard could work wonders by optimizing 7-Eleven in the US & Canada.

Seven & i’s overseas business has a wide footprint in East and Southeast Asia outside of Japan, a region in which Couche-Tard’s presence is quite light.

I’m not sure what the “right” price is for Seven & i Holdings. EBITDA during the past 3 years has been USD $6.5-$7 billion with Net Debt of ~USD $20 billion. The market capitalization is close to USD $40 billion, and the enterprise value is ~USD $60 billion as of Friday, November 15th, 2024. The EV/EBITDA multiple is close to 9x LTM, while Couche-Tard sits at close to 13x. What I do know is that, as long as Couche-Tard commits to not messing with the Japanese operations, Seven & i is worth much more in their hands than under current management.

Electric Vehicles.

The main long-term risk I see for Couche-Tard is a significant increase in the share of mobility of electric vehicles around the world, given the fact that 75% of revenues and 50% of gross profits come from fuel.

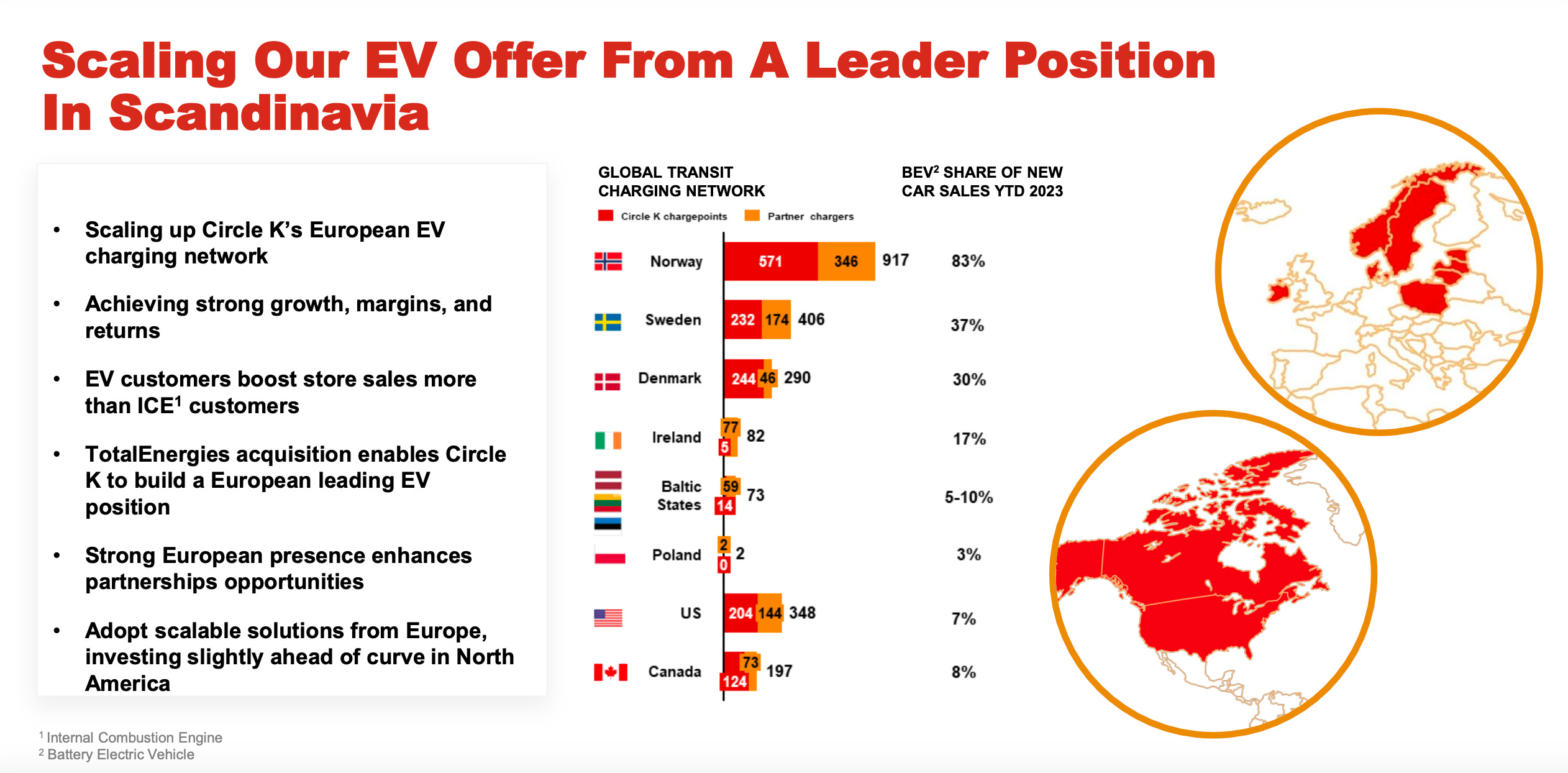

While it might not be representative, Couche-Tard does have experience offering EV charging points and services since they have been operating in Scandinavia for more than a decade. The results are encouraging as EV customers in Norway have proven to be positive contributors to traffic, sales and merchandise gross profits.

Source: ATD 2023 Analyst Conference Presentation.

Source: ATD 2023 Analyst Conference Presentation. Ultimately, the long-term financial impact of the growth in EVs on Couche-Tard is still up in the air. That said, I do think that:

The global adoption of EVs won’t be as fast as many analysts are projecting.

The adoption of EVs and consumption patterns of EV users will vary widely from one geography to the next. The US, Asia ex. China and LATAM are three regions where I think EV adoption will lag and customer dynamics will remain favorable to Couche-Tard’s operations.

Friendly reminder to do your own due diligence before making any investment decision!

Hope you enjoyed this quick article!

What is your target prize for the stock, if the deal with Seven & I finally works, what seems right now quite probable? In my model I see almost an upside of 60-80% currently.